Management: | Investor Relations: |

Stephen E. Budorick, President & CEO | Stephanie M. Krewson-Kelly, VP of IR |

Anthony Mifsud, EVP & CFO | 443-285-5453, stephanie.kelly@copt.com |

Michelle Layne, Manager of IR | |

443-285-5452, michelle.layne@copt.com | |

Firm | Senior Analyst | Phone | Email | |||

Bank of America Merrill Lynch | Jamie Feldman | 646-855-5808 | james.feldman@baml.com | |||

BTIG | Tom Catherwood | 212-738-6410 | tcatherwood@btig.com | |||

Capital One Securities | Chris Lucas | 571-633-8151 | christopher.lucas@capitalone.com | |||

Citigroup Global Markets | Manny Korchman | 212-816-1382 | emmanuel.korchman@citi.com | |||

Credit Suisse | Derek van Dijkum | 212-325-9752 | derek.vandijkum@credit-suisse.com | |||

Evercore ISI | Steve Sakwa | 212-446-9462 | steve.sakwa@evercoreisi.com | |||

Green Street Advisors | Jed Reagan | 949-640-8780 | jreagan@greenstreetadvisors.com | |||

Jefferies & Co. | Jonathan Petersen | 212-284-1705 | jpetersen@jefferies.com | |||

JP Morgan | Tony Paolone | 212-622-6682 | anthony.paolone@jpmorgan.com | |||

KeyBanc Capital Markets | Craig Mailman | 917-368-2316 | cmailman@key.com | |||

Mizuho Securities USA Inc. | Richard Anderson | 212-205-8445 | richard.anderson@us.mizuho-sc.com | |||

Raymond James | Bill Crow | 727-567-2594 | bill.crow@raymondjames.com | |||

Robert W. Baird & Co., Inc. | Dave Rodgers | 216-737-7341 | drodgers@rwbaird.com | |||

Stifel Financial Corp. | John Guinee | 443-224-1307 | jwguinee@stifel.com | |||

SunTrust Robinson Humphrey, Inc. | Michael Lewis | 212-319-5659 | michael.lewis@suntrust.com | |||

Page | Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||||

SUMMARY OF RESULTS | Refer. | 9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | ||||||||||||||||||||||

Net income (loss) | 6 | $ | 29,272 | $ | (48,316 | ) | $ | 8,096 | $ | 62,617 | $ | 94,294 | $ | (10,948 | ) | $ | 126,261 | |||||||||||||

NOI from real estate operations | 14 | $ | 82,010 | $ | 85,783 | $ | 81,212 | $ | 85,979 | $ | 84,789 | $ | 249,005 | $ | 238,601 | |||||||||||||||

Same Office Property NOI | 16 | $ | 61,295 | $ | 61,264 | $ | 59,280 | $ | 61,322 | $ | 61,589 | $ | 181,839 | $ | 179,753 | |||||||||||||||

Same Office Property Cash NOI | 17 | $ | 60,952 | $ | 61,437 | $ | 59,709 | $ | 60,928 | $ | 60,297 | $ | 182,098 | $ | 174,942 | |||||||||||||||

Adjusted EBITDA | 10 | $ | 76,834 | $ | 79,625 | $ | 74,906 | $ | 79,718 | $ | 78,932 | $ | 231,365 | $ | 220,149 | |||||||||||||||

Diluted AFFO avail. to common share and unit holders | 9 | $ | 37,998 | $ | 42,937 | $ | 36,835 | $ | 31,592 | $ | 36,570 | $ | 117,770 | $ | 115,106 | |||||||||||||||

Dividend per common share | N/A | $ | 0.275 | $ | 0.275 | $ | 0.275 | $ | 0.275 | $ | 0.275 | $ | 0.825 | $ | 0.825 | |||||||||||||||

Per share - diluted: | ||||||||||||||||||||||||||||||

EPS | 8 | $ | 0.25 | $ | (0.54 | ) | $ | 0.03 | $ | 0.59 | $ | 0.91 | $ | (0.26 | ) | $ | 1.15 | |||||||||||||

FFO - NAREIT | 8 | $ | 0.49 | $ | 0.36 | $ | 0.39 | $ | 0.31 | $ | 1.32 | $ | 1.25 | $ | 2.24 | |||||||||||||||

FFO - as adjusted for comparability | 8 | $ | 0.51 | $ | 0.52 | $ | 0.47 | $ | 0.52 | $ | 0.52 | $ | 1.50 | $ | 1.49 | |||||||||||||||

Numerators for diluted per share amounts: | ||||||||||||||||||||||||||||||

Diluted EPS | 6 | $ | 23,642 | $ | (51,068 | ) | $ | 3,156 | $ | 55,581 | $ | 86,251 | $ | (24,270 | ) | $ | 112,035 | |||||||||||||

Diluted FFO available to common share and unit holders | 7 | $ | 48,449 | $ | 35,194 | $ | 38,560 | $ | 30,488 | $ | 130,241 | $ | 122,203 | $ | 218,966 | |||||||||||||||

Diluted FFO available to common share and unit holders, as adjusted for comparability | 7 | $ | 50,461 | $ | 50,630 | $ | 46,007 | $ | 50,858 | $ | 50,684 | $ | 147,098 | $ | 144,966 | |||||||||||||||

Payout ratios: | ||||||||||||||||||||||||||||||

Diluted FFO | N/A | 55.8 | % | 76.8 | % | 70.1 | % | 88.6 | % | 21.2 | % | 66.4 | % | 37.0 | % | |||||||||||||||

Diluted FFO - as adjusted for comparability | N/A | 53.6 | % | 53.4 | % | 58.8 | % | 53.1 | % | 53.3 | % | 55.2 | % | 55.9 | % | |||||||||||||||

Diluted AFFO | N/A | 71.2 | % | 63.0 | % | 73.4 | % | 85.5 | % | 73.9 | % | 68.9 | % | 70.4 | % | |||||||||||||||

CAPITALIZATION | ||||||||||||||||||||||||||||||

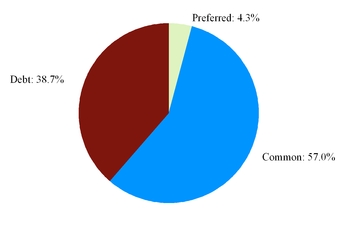

Total Market Capitalization | 29 | $ | 4,887,466 | $ | 5,228,793 | $ | 4,947,152 | $ | 4,449,015 | $ | 4,406,333 | |||||||||||||||||||

Total Equity Market Capitalization | 29 | $ | 2,996,247 | $ | 3,116,093 | $ | 2,788,272 | $ | 2,351,785 | $ | 2,273,260 | |||||||||||||||||||

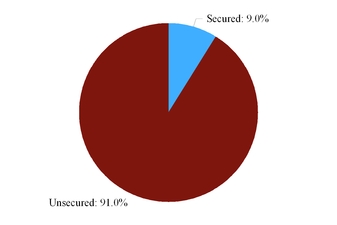

Gross debt | 30 | $ | 1,921,219 | $ | 2,112,700 | $ | 2,158,880 | $ | 2,097,230 | $ | 2,133,073 | |||||||||||||||||||

Net debt to adjusted book (1) | 32 | 41.2 | % | 43.6 | % | 43.3 | % | 42.6 | % | 43.8 | % | N/A | N/A | |||||||||||||||||

Net debt plus preferred equity to adjusted book (1) | 32 | 45.8 | % | 48.0 | % | 47.6 | % | 47.0 | % | 48.0 | % | N/A | N/A | |||||||||||||||||

Adjusted EBITDA fixed charge coverage ratio | 32 | 3.1 | x | 2.9 | x | 2.7 | x | 2.9 | x | 2.9 | x | 2.9 | x | 3.0 | x | |||||||||||||||

Net debt to in-place adjusted EBITDA ratio | 32 | 6.3 | x | 6.6 | x | 7.0 | x | 6.5 | x | 6.6 | x | N/A | N/A | |||||||||||||||||

Net debt plus pref. equity to in-place adj. EBITDA ratio | 32 | 7.0 | x | 7.2 | x | 7.6 | x | 7.2 | x | 7.3 | x | N/A | N/A | |||||||||||||||||

OTHER | ||||||||||||||||||||||||||||||

Revenue from early termination of leases | N/A | $ | 437 | $ | 338 | $ | 712 | $ | 400 | $ | 159 | $ | 1,487 | $ | 1,423 | |||||||||||||||

Capitalized interest costs | N/A | $ | 1,242 | $ | 1,309 | $ | 1,753 | $ | 1,510 | $ | 1,559 | $ | 4,304 | $ | 5,641 | |||||||||||||||

(1) | Effective this quarter, we commenced reporting for these ratios in lieu of debt to adjusted book. Please refer to to the section entitled “Definitions” for additional information regarding these ratios. |

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | ||||||||||

(1) | ||||||||||||||

# of Operating Office Properties | ||||||||||||||

Total Portfolio | 168 | 181 | 179 | 177 | 183 | |||||||||

Consolidated Portfolio | 162 | 181 | 179 | 177 | 183 | |||||||||

Core Portfolio | 146 | 146 | 153 | 157 | 164 | |||||||||

Same Office Properties | 129 | 129 | 129 | 129 | 129 | |||||||||

% Occupied | ||||||||||||||

Total Portfolio | 91.3 | % | 92.6 | % | 92.3 | % | 92.7 | % | 92.3 | % | ||||

Consolidated Portfolio | 90.8 | % | 92.6 | % | 92.3 | % | 92.7 | % | 92.3 | % | ||||

Core Portfolio | 93.0 | % | 92.3 | % | 91.6 | % | 92.7 | % | 91.3 | % | ||||

Same Office Properties | 91.4 | % | 91.1 | % | 90.7 | % | 91.6 | % | 91.3 | % | ||||

% Leased | ||||||||||||||

Total Portfolio | 92.8 | % | 92.6 | % | 92.3 | % | 92.7 | % | 92.3 | % | ||||

Consolidated Portfolio | 92.4 | % | 92.6 | % | 92.3 | % | 92.7 | % | 92.3 | % | ||||

Core Portfolio | 94.4 | % | 93.8 | % | 93.3 | % | 93.9 | % | 92.1 | % | ||||

Same Office Properties | 93.2 | % | 92.7 | % | 92.5 | % | 93.0 | % | 92.0 | % | ||||

Square Feet of Office Properties (in thousands) | ||||||||||||||

Total Portfolio | 17,488 | 18,402 | 18,250 | 18,053 | 18,825 | |||||||||

Consolidated Portfolio | 16,526 | 18,402 | 18,250 | 18,053 | 18,825 | |||||||||

Core Portfolio | 15,938 | 16,018 | 16,556 | 17,038 | 17,515 | |||||||||

Same Office Properties | 13,041 | 13,041 | 13,041 | 13,041 | 13,041 | |||||||||

Wholesale Data Center (in megawatts (“MWs”)) | ||||||||||||||

Initial Stabilization Critical Load | 19.25 | 19.25 | 19.25 | 19.25 | 19.25 | |||||||||

MWs Leased (2) | 15.81 | 15.81 | 16.81 | 17.81 | 17.81 | |||||||||

MWs Operational | 19.25 | 19.25 | 19.25 | 19.25 | 19.25 | |||||||||

(1) | As of 9/30/2016, our total portfolio included 19 properties held for sale totaling 1.3 million square feet that were 81.3% occupied and 84.0% leased. Our total portfolio and core portfolio included six properties owned through an unconsolidated joint venture totaling 962,000 square feet that were 100% occupied and leased. |

(2) | Leased to tenants with further expansion rights of up to a combined 16.87 megawatts as of September 30, 2016. |

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | |||||||||||||||

Assets | |||||||||||||||||||

Properties, net | |||||||||||||||||||

Operating properties, net | $ | 2,632,069 | $ | 2,782,330 | $ | 2,863,262 | $ | 2,920,529 | $ | 2,932,843 | |||||||||

Construction and redevelopment in progress, including land (1) | 72,043 | 69,070 | 98,198 | 137,043 | 77,268 | ||||||||||||||

Land held (1) | 324,226 | 318,327 | 317,971 | 292,176 | 337,489 | ||||||||||||||

Total properties, net | 3,028,338 | 3,169,727 | 3,279,431 | 3,349,748 | 3,347,600 | ||||||||||||||

Assets held for sale | 161,454 | 300,584 | 225,897 | 96,782 | 150,572 | ||||||||||||||

Cash and cash equivalents | 47,574 | 13,317 | 62,489 | 60,310 | 3,840 | ||||||||||||||

Restricted cash and marketable securities | 7,583 | 8,302 | 7,763 | 7,716 | 9,286 | ||||||||||||||

Investment in unconsolidated real estate joint venture | 25,721 | — | — | — | — | ||||||||||||||

Accounts receivable, net | 25,790 | 32,505 | 28,776 | 29,167 | 23,706 | ||||||||||||||

Deferred rent receivable, net | 87,526 | 92,316 | 96,936 | 105,484 | 103,064 | ||||||||||||||

Intangible assets on real estate acquisitions, net | 84,081 | 88,788 | 93,526 | 98,338 | 106,174 | ||||||||||||||

Deferred leasing costs, net | 41,470 | 42,632 | 44,768 | 53,868 | 51,509 | ||||||||||||||

Investing receivables | 51,119 | 50,162 | 48,998 | 47,875 | 46,821 | ||||||||||||||

Prepaid expenses and other assets, net | 73,538 | 43,359 | 49,324 | 60,024 | 69,520 | ||||||||||||||

Total assets | $ | 3,634,194 | $ | 3,841,692 | $ | 3,937,908 | $ | 3,909,312 | $ | 3,912,092 | |||||||||

Liabilities and equity | |||||||||||||||||||

Liabilities: | |||||||||||||||||||

Debt | $ | 1,873,836 | $ | 2,094,486 | $ | 2,140,212 | $ | 2,077,752 | $ | 2,114,859 | |||||||||

Accounts payable and accrued expenses | 112,306 | 92,848 | 78,597 | 91,755 | 98,551 | ||||||||||||||

Rents received in advance and security deposits | 28,740 | 32,035 | 33,457 | 37,148 | 34,504 | ||||||||||||||

Dividends and distributions payable | 30,225 | 30,219 | 30,217 | 30,178 | 30,182 | ||||||||||||||

Deferred revenue associated with operating leases | 9,898 | 17,560 | 19,093 | 19,758 | 20,113 | ||||||||||||||

Interest rate derivatives | 17,272 | 20,245 | 15,072 | 3,160 | 5,844 | ||||||||||||||

Other liabilities | 38,282 | 31,123 | 15,046 | 13,779 | 8,524 | ||||||||||||||

Total liabilities | 2,110,559 | 2,318,516 | 2,331,694 | 2,273,530 | 2,312,577 | ||||||||||||||

Redeemable noncontrolling interests | 22,848 | 22,473 | 22,333 | 19,218 | 19,608 | ||||||||||||||

Equity: | |||||||||||||||||||

COPT’s shareholders’ equity: | |||||||||||||||||||

Preferred shares at liquidation preference | 199,083 | 199,083 | 199,083 | 199,083 | 199,083 | ||||||||||||||

Common shares | 948 | 947 | 947 | 945 | 945 | ||||||||||||||

Additional paid-in capital | 2,008,787 | 2,007,328 | 2,005,523 | 2,004,507 | 2,002,730 | ||||||||||||||

Cumulative distributions in excess of net income | (759,262 | ) | (756,940 | ) | (679,935 | ) | (657,172 | ) | (686,986 | ) | |||||||||

Accumulated other comprehensive loss | (16,314 | ) | (17,712 | ) | (12,862 | ) | (2,838 | ) | (5,823 | ) | |||||||||

Total COPT’s shareholders’ equity | 1,433,242 | 1,432,706 | 1,512,756 | 1,544,525 | 1,509,949 | ||||||||||||||

Noncontrolling interests in subsidiaries | |||||||||||||||||||

Common units in the Operating Partnership | 46,757 | 47,550 | 51,031 | 52,359 | 50,992 | ||||||||||||||

Preferred units in the Operating Partnership | 8,800 | 8,800 | 8,800 | 8,800 | 8,800 | ||||||||||||||

Other consolidated entities | 11,988 | 11,647 | 11,294 | 10,880 | 10,166 | ||||||||||||||

Total noncontrolling interests in subsidiaries | 67,545 | 67,997 | 71,125 | 72,039 | 69,958 | ||||||||||||||

Total equity | 1,500,787 | 1,500,703 | 1,583,881 | 1,616,564 | 1,579,907 | ||||||||||||||

Total liabilities, redeemable noncontrolling interest and equity | $ | 3,634,194 | $ | 3,841,692 | $ | 3,937,908 | $ | 3,909,312 | $ | 3,912,092 | |||||||||

(1) Please refer to pages 24-26 and 28 for detail. | |||||||||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | |||||||||||||||||||||

Revenues | |||||||||||||||||||||||||||

Rental revenue | $ | 103,956 | $ | 107,524 | $ | 105,382 | $ | 107,514 | $ | 109,080 | $ | 316,862 | $ | 312,826 | |||||||||||||

Tenant recoveries and other real estate operations revenue | 26,998 | 26,400 | 27,705 | 26,963 | 24,606 | 81,103 | 71,761 | ||||||||||||||||||||

Construction contract and other service revenues | 11,149 | 12,003 | 11,220 | 8,848 | 17,058 | 34,372 | 97,554 | ||||||||||||||||||||

Total revenues | 142,103 | 145,927 | 144,307 | 143,325 | 150,744 | 432,337 | 482,141 | ||||||||||||||||||||

Expenses | |||||||||||||||||||||||||||

Property operating expenses | 49,952 | 48,141 | 51,875 | 48,498 | 48,897 | 149,968 | 145,996 | ||||||||||||||||||||

Depreciation and amortization associated with real estate operations | 32,015 | 33,248 | 34,527 | 36,237 | 38,403 | 99,790 | 103,788 | ||||||||||||||||||||

Construction contract and other service expenses | 10,341 | 11,478 | 10,694 | 7,773 | 16,132 | 32,513 | 94,923 | ||||||||||||||||||||

Impairment losses | 27,699 | 69,692 | 2,446 | 19,744 | 2,307 | 99,837 | 3,545 | ||||||||||||||||||||

General and administrative expenses | 7,242 | 6,512 | 10,130 | 6,609 | 5,783 | 23,884 | 17,917 | ||||||||||||||||||||

Leasing expenses | 1,613 | 1,514 | 1,753 | 1,888 | 1,656 | 4,880 | 4,947 | ||||||||||||||||||||

Business development expenses and land carry costs | 1,716 | 2,363 | 2,418 | 2,521 | 5,573 | 6,497 | 10,986 | ||||||||||||||||||||

Total operating expenses | 130,578 | 172,948 | 113,843 | 123,270 | 118,751 | 417,369 | 382,102 | ||||||||||||||||||||

Operating income (loss) | 11,525 | (27,021 | ) | 30,464 | 20,055 | 31,993 | 14,968 | 100,039 | |||||||||||||||||||

Interest expense | (18,301 | ) | (22,639 | ) | (23,559 | ) | (22,347 | ) | (24,121 | ) | (64,499 | ) | (66,727 | ) | |||||||||||||

Interest and other income | 1,391 | 1,330 | 1,156 | 1,300 | 692 | 3,877 | 3,217 | ||||||||||||||||||||

(Loss) gain on early extinguishment of debt | (59 | ) | 5 | 17 | (402 | ) | 85,745 | (37 | ) | 85,677 | |||||||||||||||||

(Loss) income from continuing operations before equity in income of unconsolidated entities and income taxes | (5,444 | ) | (48,325 | ) | 8,078 | (1,394 | ) | 94,309 | (45,691 | ) | 122,206 | ||||||||||||||||

Equity in income of unconsolidated entities | 594 | 10 | 10 | 10 | 18 | 614 | 52 | ||||||||||||||||||||

Income tax benefit (expense) | 21 | (1 | ) | 8 | (46 | ) | (48 | ) | 28 | (153 | ) | ||||||||||||||||

(Loss) income from continuing operations | (4,829 | ) | (48,316 | ) | 8,096 | (1,430 | ) | 94,279 | (45,049 | ) | 122,105 | ||||||||||||||||

Discontinued operations | — | — | — | — | — | — | 156 | ||||||||||||||||||||

(Loss) income before gain on sales of real estate | (4,829 | ) | (48,316 | ) | 8,096 | (1,430 | ) | 94,279 | (45,049 | ) | 122,261 | ||||||||||||||||

Gain on sales of real estate | 34,101 | — | — | 64,047 | 15 | 34,101 | 4,000 | ||||||||||||||||||||

Net income (loss) | 29,272 | (48,316 | ) | 8,096 | 62,617 | 94,294 | (10,948 | ) | 126,261 | ||||||||||||||||||

Net (income) loss attributable to noncontrolling interests | |||||||||||||||||||||||||||

Common units in the Operating Partnership | (901 | ) | 1,976 | (127 | ) | (2,172 | ) | (3,357 | ) | 948 | (4,231 | ) | |||||||||||||||

Preferred units in the Operating Partnership | (165 | ) | (165 | ) | (165 | ) | (165 | ) | (165 | ) | (495 | ) | (495 | ) | |||||||||||||

Other consolidated entities | (907 | ) | (914 | ) | (978 | ) | (916 | ) | (972 | ) | (2,799 | ) | (2,599 | ) | |||||||||||||

Net income (loss) attributable to COPT | 27,299 | (47,419 | ) | 6,826 | 59,364 | 89,800 | (13,294 | ) | 118,936 | ||||||||||||||||||

Preferred share dividends | (3,552 | ) | (3,553 | ) | (3,552 | ) | (3,553 | ) | (3,552 | ) | (10,657 | ) | (10,657 | ) | |||||||||||||

Net income (loss) attributable to COPT common shareholders | $ | 23,747 | $ | (50,972 | ) | $ | 3,274 | $ | 55,811 | $ | 86,248 | $ | (23,951 | ) | $ | 108,279 | |||||||||||

Dividends on dilutive convertible preferred shares | — | — | — | — | 372 | — | — | ||||||||||||||||||||

Common units in the Operating Partnership | — | — | — | — | — | — | 4,231 | ||||||||||||||||||||

Amount allocable to share-based compensation awards | (105 | ) | (96 | ) | (118 | ) | (230 | ) | (369 | ) | (319 | ) | (475 | ) | |||||||||||||

Numerator for diluted EPS | $ | 23,642 | $ | (51,068 | ) | $ | 3,156 | $ | 55,581 | $ | 86,251 | $ | (24,270 | ) | $ | 112,035 | |||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | |||||||||||||||||||||

Net income (loss) | $ | 29,272 | $ | (48,316 | ) | $ | 8,096 | $ | 62,617 | $ | 94,294 | $ | (10,948 | ) | $ | 126,261 | |||||||||||

Real estate-related depreciation and amortization | 32,015 | 33,248 | 34,527 | 36,237 | 38,403 | 99,790 | 103,788 | ||||||||||||||||||||

Impairment losses on previously depreciated operating properties | 25,857 | 55,124 | 847 | 331 | 2,307 | 81,828 | 3,779 | ||||||||||||||||||||

Gain on sales of previously depreciated operating properties | (34,101 | ) | — | — | (64,047 | ) | (15 | ) | (34,101 | ) | (15 | ) | |||||||||||||||

Depreciation and amortization on unconsolidated real estate JV (1) | 207 | — | — | — | — | 207 | — | ||||||||||||||||||||

FFO - per NAREIT (2)(3) | 53,250 | 40,056 | 43,470 | 35,138 | 134,989 | 136,776 | 233,813 | ||||||||||||||||||||

Preferred share dividends | (3,552 | ) | (3,553 | ) | (3,552 | ) | (3,553 | ) | (3,552 | ) | (10,657 | ) | (10,657 | ) | |||||||||||||

Noncontrolling interests - preferred units in the Operating Partnership | (165 | ) | (165 | ) | (165 | ) | (165 | ) | (165 | ) | (495 | ) | (495 | ) | |||||||||||||

FFO allocable to other noncontrolling interests (4) | (894 | ) | (1,014 | ) | (1,027 | ) | (817 | ) | (1,027 | ) | (2,935 | ) | (2,769 | ) | |||||||||||||

Basic and diluted FFO allocable to restricted shares | (190 | ) | (130 | ) | (166 | ) | (115 | ) | (541 | ) | (486 | ) | (926 | ) | |||||||||||||

Basic FFO available to common share and common unit holders (3) | 48,449 | 35,194 | 38,560 | 30,488 | 129,704 | 122,203 | 218,966 | ||||||||||||||||||||

Dividends on dilutive convertible preferred shares | — | — | — | — | 372 | — | — | ||||||||||||||||||||

Distributions on dilutive preferred units in the Operating Partnership | — | — | — | — | 165 | — | — | ||||||||||||||||||||

Diluted FFO available to common share and common unit holders (3) | 48,449 | 35,194 | 38,560 | 30,488 | 130,241 | 122,203 | 218,966 | ||||||||||||||||||||

Operating property acquisition costs | — | — | — | 32 | 2,695 | — | 4,102 | ||||||||||||||||||||

Gain on sales of non-operating properties | — | — | — | — | — | — | (3,985 | ) | |||||||||||||||||||

Impairment losses on non-operating properties | 1,842 | 14,568 | 1,599 | 19,413 | — | 18,009 | — | ||||||||||||||||||||

(Gain) loss on interest rate derivatives | (1,523 | ) | 319 | 1,551 | 386 | — | 347 | — | |||||||||||||||||||

Loss (gain) on early extinguishment of debt | 59 | (5 | ) | (17 | ) | 402 | (85,745 | ) | 37 | (86,057 | ) | ||||||||||||||||

Add: Negative FFO of properties conveyed to extinguish debt in default (5) | — | — | — | — | 2,766 | — | 10,456 | ||||||||||||||||||||

Demolition costs on redevelopment properties | — | 370 | 208 | 225 | 930 | 578 | 1,171 | ||||||||||||||||||||

Executive transition costs | 1,639 | 247 | 4,137 | — | — | 6,023 | — | ||||||||||||||||||||

Diluted FFO comparability adjustments allocable to restricted shares | (5 | ) | (63 | ) | (31 | ) | (88 | ) | 334 | (99 | ) | 313 | |||||||||||||||

Dividends and distributions on antidilutive preferred securities (6) | — | — | — | — | (537 | ) | — | — | |||||||||||||||||||

Diluted FFO avail. to common share and common unit holders, as adj. for comparability (3) | $ | 50,461 | $ | 50,630 | $ | 46,007 | $ | 50,858 | $ | 50,684 | $ | 147,098 | $ | 144,966 | |||||||||||||

(1) FFO adjustment pertaining to COPT’s share of an unconsolidated real estate joint venture reported on page 34. | |||||||||||||||||||||||||||

(2) Please see reconciliation on page 36 for components of FFO per NAREIT. | |||||||||||||||||||||||||||

(3) Please refer to the section entitled “Definitions” for a definition of this measure. | |||||||||||||||||||||||||||

(4) Pertains to noncontrolling interests in consolidated real estate joint ventures reported on page 33. | |||||||||||||||||||||||||||

(5) Interest expense exceeded NOI from these properties by the amounts in the statement. | |||||||||||||||||||||||||||

(6) These securities were dilutive for Diluted FFO purposes but antidilutive for Diluted FFO as adjusted for comparability purposes. | |||||||||||||||||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | |||||||||||||||||||||

EPS Denominator: | |||||||||||||||||||||||||||

Weighted average common shares - basic | 94,433 | 94,300 | 94,203 | 94,164 | 94,153 | 94,312 | 93,830 | ||||||||||||||||||||

Dilutive convertible preferred shares | — | — | — | — | 434 | — | — | ||||||||||||||||||||

Common units in the Operating Partnership | — | — | — | — | — | — | 3,697 | ||||||||||||||||||||

Dilutive effect of share-based compensation awards | 81 | — | 95 | — | 21 | — | 82 | ||||||||||||||||||||

Weighted average common shares - diluted | 94,514 | 94,300 | 94,298 | 94,164 | 94,608 | 94,312 | 97,609 | ||||||||||||||||||||

Diluted EPS | $ | 0.25 | $ | (0.54 | ) | $ | 0.03 | $ | 0.59 | $ | 0.91 | $ | (0.26 | ) | $ | 1.15 | |||||||||||

Weighted Average Shares for period ended: | |||||||||||||||||||||||||||

Common Shares Outstanding | 94,433 | 94,300 | 94,203 | 94,164 | 94,153 | 94,312 | 93,830 | ||||||||||||||||||||

Dilutive effect of share-based compensation awards | 81 | 117 | 95 | — | 21 | 98 | 82 | ||||||||||||||||||||

Common Units | 3,591 | 3,676 | 3,677 | 3,677 | 3,679 | 3,648 | 3,697 | ||||||||||||||||||||

Dilutive convertible preferred shares (1) | — | — | — | — | 434 | — | — | ||||||||||||||||||||

Dilutive noncontrolling interests - preferred units in the Operating Partnership (1) | — | — | — | — | 176 | — | — | ||||||||||||||||||||

Denominator for diluted FFO per share | 98,105 | 98,093 | 97,975 | 97,841 | 98,463 | 98,058 | 97,609 | ||||||||||||||||||||

Antidilutive preferred securities for diluted FFO, as adjusted for comparability (1) | — | — | — | — | (610 | ) | — | — | |||||||||||||||||||

Denominator for diluted FFO per share, as adjusted for comparability | 98,105 | 98,093 | 97,975 | 97,841 | 97,853 | 98,058 | 97,609 | ||||||||||||||||||||

Weighted average common units | (3,591 | ) | (3,676 | ) | (3,677 | ) | (3,677 | ) | (3,679 | ) | (3,648 | ) | — | ||||||||||||||

Anti-dilutive EPS effect of share-based compensation awards | — | (117 | ) | — | — | — | (98 | ) | — | ||||||||||||||||||

Dilutive convertible preferred shares | — | — | — | — | 434 | — | — | ||||||||||||||||||||

Denominator for diluted EPS | 94,514 | 94,300 | 94,298 | 94,164 | 94,608 | 94,312 | 97,609 | ||||||||||||||||||||

Diluted FFO per share - NAREIT | $ | 0.49 | $ | 0.36 | $ | 0.39 | $ | 0.31 | $ | 1.32 | $ | 1.25 | $ | 2.24 | |||||||||||||

Diluted FFO per share - as adjusted for comparability | $ | 0.51 | $ | 0.52 | $ | 0.47 | $ | 0.52 | $ | 0.52 | $ | 1.50 | $ | 1.49 | |||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | |||||||||||||||||||||

Diluted FFO available to common share and common unit holders, as adjusted for comparability | $ | 50,461 | $ | 50,630 | $ | 46,007 | $ | 50,858 | $ | 50,684 | $ | 147,098 | $ | 144,966 | |||||||||||||

Straight line rent adjustments and lease incentive amortization | 691 | 480 | (965 | ) | (2,677 | ) | (5,625 | ) | 206 | (10,820 | ) | ||||||||||||||||

Straight line rent adjustments on properties conveyed to extinguish debt in default | — | — | — | — | (19 | ) | — | (115 | ) | ||||||||||||||||||

Amortization of intangibles included in NOI | 349 | 338 | 338 | 365 | 474 | 1,025 | 1,063 | ||||||||||||||||||||

Share-based compensation, net of amounts capitalized | 1,258 | 1,485 | 1,632 | 1,625 | 1,739 | 4,375 | 4,949 | ||||||||||||||||||||

Amortization of deferred financing costs | 1,126 | 1,178 | 1,176 | 1,127 | 1,203 | 3,480 | 3,339 | ||||||||||||||||||||

Amortization of net debt discounts, net of amounts capitalized | 332 | 325 | 319 | 317 | 321 | 976 | 849 | ||||||||||||||||||||

Replacement capital expenditures (1) | (16,120 | ) | (11,546 | ) | (11,720 | ) | (20,086 | ) | (12,126 | ) | (39,386 | ) | (29,180 | ) | |||||||||||||

Diluted AFFO adjustments allocable to other noncontrolling interests (2) | 42 | 47 | 48 | 63 | (81 | ) | 137 | 55 | |||||||||||||||||||

Diluted AFFO adjustments on unconsolidated real estate JV (3) | (141 | ) | — | — | — | — | (141 | ) | — | ||||||||||||||||||

Diluted AFFO available to common share and common unit holders (“diluted AFFO”) | $ | 37,998 | $ | 42,937 | $ | 36,835 | $ | 31,592 | $ | 36,570 | $ | 117,770 | $ | 115,106 | |||||||||||||

Replacement capital expenditures (1) | |||||||||||||||||||||||||||

Tenant improvements and incentives | $ | 21,470 | $ | 6,784 | $ | 8,766 | $ | 6,836 | $ | 6,374 | $ | 37,020 | $ | 17,408 | |||||||||||||

Building improvements | 5,707 | 5,302 | 3,953 | 16,674 | 4,223 | 14,962 | 11,969 | ||||||||||||||||||||

Leasing costs | 5,182 | 1,613 | 1,183 | 3,518 | 2,547 | 7,978 | 4,986 | ||||||||||||||||||||

Less: Excluded tenant improvements and incentives | (12,706 | ) | (885 | ) | (1,353 | ) | (393 | ) | 205 | (14,944 | ) | (1,045 | ) | ||||||||||||||

Less: Excluded building improvements | (3,533 | ) | (1,121 | ) | (557 | ) | (6,551 | ) | (1,155 | ) | (5,211 | ) | (3,328 | ) | |||||||||||||

Less: Excluded leasing costs | — | (147 | ) | (272 | ) | 2 | (68 | ) | (419 | ) | (810 | ) | |||||||||||||||

Replacement capital expenditures | $ | 16,120 | $ | 11,546 | $ | 11,720 | $ | 20,086 | $ | 12,126 | $ | 39,386 | $ | 29,180 | |||||||||||||

(1) Please refer to the section entitled “Definitions” for a definition of this measure. | |||||||||||||||||||||||||||

(2) AFFO adjustments pertaining to noncontrolling interests on consolidated joint ventures reported on page 33. | |||||||||||||||||||||||||||

(3) AFFO adjustments pertaining to COPT’s share of an unconsolidated real estate joint venture reported on page 34. | |||||||||||||||||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | |||||||||||||||||||||

Net income (loss) | $ | 29,272 | $ | (48,316 | ) | $ | 8,096 | $ | 62,617 | $ | 94,294 | $ | (10,948 | ) | $ | 126,261 | |||||||||||

Interest expense on continuing and discontinued operations | 18,301 | 22,639 | 23,559 | 22,347 | 24,121 | 64,499 | 66,727 | ||||||||||||||||||||

Income tax (benefit) expense | (21 | ) | 1 | (8 | ) | 46 | 48 | (28 | ) | 153 | |||||||||||||||||

Depreciation of furniture, fixtures and equipment | 513 | 524 | 602 | 597 | 590 | 1,639 | 1,609 | ||||||||||||||||||||

Real estate-related depreciation and amortization | 32,015 | 33,248 | 34,527 | 36,237 | 38,403 | 99,790 | 103,788 | ||||||||||||||||||||

Impairment losses | 27,699 | 69,692 | 2,446 | 19,744 | 2,307 | 99,837 | 3,779 | ||||||||||||||||||||

Loss (gain) on early extinguishment of debt on continuing and discontinued operations | 59 | (5 | ) | (17 | ) | 402 | (85,745 | ) | 37 | (86,057 | ) | ||||||||||||||||

Gain on sales of operating properties | (34,101 | ) | — | — | (64,047 | ) | (15 | ) | (34,101 | ) | (15 | ) | |||||||||||||||

Gain on sales of non-operational properties | — | — | — | — | — | — | (3,985 | ) | |||||||||||||||||||

Net loss (gain) on investments in unconsolidated entities included in interest and other income | 27 | (36 | ) | (23 | ) | 6 | 98 | (32 | ) | 121 | |||||||||||||||||

Business development expenses | 1,016 | 1,261 | 1,379 | 1,512 | 1,221 | 3,656 | 3,263 | ||||||||||||||||||||

Operating property acquisition costs | — | — | — | 32 | 2,695 | — | 4,102 | ||||||||||||||||||||

EBITDA from properties conveyed to extinguish debt in default | — | — | — | — | (15 | ) | — | (768 | ) | ||||||||||||||||||

Demolition costs on redevelopment properties | — | 370 | 208 | 225 | 930 | 578 | 1,171 | ||||||||||||||||||||

Adjustments from unconsolidated real estate JV (1) | 415 | — | — | — | — | 415 | — | ||||||||||||||||||||

Executive transition costs | 1,639 | 247 | 4,137 | — | — | 6,023 | — | ||||||||||||||||||||

Adjusted EBITDA | $ | 76,834 | $ | 79,625 | $ | 74,906 | $ | 79,718 | $ | 78,932 | $ | 231,365 | $ | 220,149 | |||||||||||||

Proforma NOI adjustment for property changes within period | (2,469 | ) | 109 | 471 | (1,738 | ) | 1,309 | ||||||||||||||||||||

In-place adjusted EBITDA | $ | 74,365 | $ | 79,734 | $ | 75,377 | $ | 77,980 | $ | 80,241 | |||||||||||||||||

Operational Properties (5) | Construction/Redevelopment (7) | |||||||||||||||||||||||

# of Properties | Operational Square Feet | Occupancy % | Leased % | # of Properties | Construction/Redevelopment Square Feet | Operational Square Feet (6) | Total Square Feet | |||||||||||||||||

Core Portfolio: (2) | ||||||||||||||||||||||||

Defense IT Locations: (3) | ||||||||||||||||||||||||

Fort Meade/Baltimore Washington (“BW”) Corridor: | ||||||||||||||||||||||||

National Business Park | 29 | 3,485 | 95.7 | % | 96.6 | % | 2 | 336 | 336 | |||||||||||||||

Howard County | 35 | 2,752 | 91.6 | % | 93.6 | % | 1 | 18 | 4 | 22 | ||||||||||||||

Other | 17 | 1,363 | 94.9 | % | 96.0 | % | 2 | 82 | 82 | |||||||||||||||

Total Fort Meade/BW Corridor | 81 | 7,600 | 94.1 | % | 95.4 | % | 5 | 436 | 4 | 440 | ||||||||||||||

Northern Virginia (“NoVA”) Defense/IT | 11 | 1,599 | 83.5 | % | 87.4 | % | 2 | 401 | 401 | |||||||||||||||

Lackland AFB (San Antonio, Texas) | 7 | 953 | 100.0 | % | 100.0 | % | — | — | — | — | ||||||||||||||

Navy Support | 21 | 1,261 | 73.6 | % | 78.1 | % | — | — | — | — | ||||||||||||||

Redstone Arsenal (Huntsville, Alabama) | 7 | 642 | 100.0 | % | 100.0 | % | 1 | 8 | 11 | 19 | ||||||||||||||

Data Center Shells | ||||||||||||||||||||||||

Consolidated Properties | 6 | 897 | 100.0 | % | 100.0 | % | 2 | 365 | 365 | |||||||||||||||

Unconsolidated JV Properties (4) | 6 | 962 | 100.0 | % | 100.0 | % | ||||||||||||||||||

Total Defense/IT Locations | 139 | 13,914 | 92.5 | % | 94.1 | % | 10 | 1,210 | 15 | 1,225 | ||||||||||||||

Regional Office (5) | 7 | 2,024 | 96.2 | % | 96.8 | % | — | — | — | — | ||||||||||||||

Core Portfolio | 146 | 15,938 | 93.0 | % | 94.4 | % | 10 | 1,210 | 15 | 1,225 | ||||||||||||||

Properties Held for Sale | 19 | 1,264 | 81.3 | % | 84.0 | % | — | — | — | — | ||||||||||||||

Other Properties | 3 | 286 | 44.0 | % | 44.0 | % | — | — | — | — | ||||||||||||||

Total Portfolio | 168 | 17,488 | 91.3 | % | 92.8 | % | 10 | 1,210 | 15 | 1,225 | ||||||||||||||

Consolidated Properties | 162 | 16,526 | 90.8 | % | 92.4 | % | 10 | 1,210 | 15 | 1,225 | ||||||||||||||

(1) | This presentation sets forth Core Portfolio data by segment followed by data for the remainder of the portfolio. |

(2) | Represents Defense/IT Locations and Regional Office properties excluding properties held for sale. |

(3) | Includes properties in locations that support United States Government agencies and their contractors, most of whom are engaged in national security, defense and IT related activities servicing what we believe are growing, durable, priority missions. |

(4) | See page 34 for additional disclosure regarding an unconsolidated real estate joint venture. |

(5) | Includes office properties located in select urban/urban-like submarkets within our regional footprint with durable Class-A office fundamentals and characteristics. |

(6) | Number of properties includes buildings under construction or redevelopment once those buildings become partially operational. Operational square feet includes square feet in operations for two partially operational properties; NOI and cash NOI for these properties was $19,000 for the three months ended 9/30/16. |

(7) | This schedule includes properties under, or contractually committed for, construction or redevelopment as of 9/30/16 and 310 Sentinel Way and NOVA Office B, properties that were complete but are held for future lease to the United States Government. Please refer to pages 25 and 26. |

9/30/16 | |||||||||||||||||||||||||

# of Operating Office Properties | Office Operational Square Feet | Office Property Annualized Rental Revenue (2) | Percentage of Total Office Annualized Rental Revenue (2) | NOI from Real Estate Operations for Three Months Ended | NOI from Real Estate Operations for Nine Months Ended | ||||||||||||||||||||

Property Grouping | % Occupied (1) | % Leased (1) | 9/30/16 | 9/30/16 | |||||||||||||||||||||

Core Portfolio: | |||||||||||||||||||||||||

Same Office Properties (3) | 126 | 12,755 | 92.5% | 94.3% | $ | 380,062 | 80.6 | % | $ | 60,689 | $ | 180,168 | |||||||||||||

Office Properties Placed in Service (4) | 11 | 1,048 | 89.5% | 89.5% | 23,430 | 5.0 | % | 4,261 | 11,323 | ||||||||||||||||

Acquired Office Properties (5) | 3 | 1,173 | 95.5% | 95.5% | 33,935 | 7.2 | % | 4,890 | 15,754 | ||||||||||||||||

Unconsolidated real estate JV (6) | 6 | 962 | 100.0% | 100.0% | 5,233 | 1.1 | % | 1,008 | 1,008 | ||||||||||||||||

Wholesale Data Center and Other | N/A | N/A | N/A | N/A | N/A | N/A | 3,195 | 11,120 | |||||||||||||||||

Total Core Portfolio | 146 | 15,938 | 93.0% | 94.4% | 442,660 | 93.9 | % | 74,043 | 219,373 | ||||||||||||||||

Office Properties Held for Sale (7) | 19 | 1,264 | 81.3% | 84.0% | 25,256 | 5.3 | % | 4,161 | 11,519 | ||||||||||||||||

Disposed Office Properties | N/A | N/A | N/A | N/A | N/A | N/A | 3,200 | 16,442 | |||||||||||||||||

Other Office Properties (Same Office) | 3 | 286 | 44.0% | 44.0% | 3,641 | 0.8 | % | 606 | 1,671 | ||||||||||||||||

Total Portfolio | 168 | 17,488 | 91.3% | 92.8% | $ | 471,557 | 100.0 | % | $ | 82,010 | $ | 249,005 | |||||||||||||

Consolidated Properties | 162 | 16,526 | 90.8% | 92.4% | $ | 466,324 | 98.9 | % | $ | 81,002 | $ | 247,997 | |||||||||||||

9/30/16 | |||||||||||||||||||||||||

# of Operating Office Properties | Office Operational Square Feet | Office Property Annualized Rental Revenue (2) | Percentage of Core Portfolio Annualized Rental Revenue (2) | NOI from Real Estate Operations for Three Months Ended | NOI from Real Estate Operations for Nine Months Ended | ||||||||||||||||||||

Property Grouping | % Occupied (1) | % Leased (1) | 9/30/16 | 9/30/16 | |||||||||||||||||||||

Core Portfolio: | |||||||||||||||||||||||||

Defense/IT Locations | |||||||||||||||||||||||||

Consolidated properties | 133 | 12,952 | 91.9% | 93.6% | 374,965 | 84.7 | % | 60,155 | 177,853 | ||||||||||||||||

Unconsolidated real estate JV (6) | 6 | 962 | 100.0% | 100.0% | 5,233 | 1.2 | % | 1,008 | 1,008 | ||||||||||||||||

Total Defense/IT Locations | 139 | 13,914 | 92.5% | 94.1% | 380,198 | 85.9 | % | 61,163 | 178,861 | ||||||||||||||||

Regional Office | 7 | 2,024 | 96.2% | 96.8% | 62,462 | 14.1 | % | 9,336 | 28,882 | ||||||||||||||||

Wholesale Data Center and Other | N/A | N/A | N/A | N/A | N/A | N/A | 3,544 | 11,630 | |||||||||||||||||

Total Core Portfolio | 146 | 15,938 | 93.0% | 94.4% | $ | 442,660 | 100.0 | % | $ | 74,043 | $ | 219,373 | |||||||||||||

(1) | Percentages calculated based on operational square feet. |

(2) | Excludes Annualized Rental Revenue from our wholesale data center, DC-6, of $20.5 million as of 9/30/16. With regard to properties owned through unconsolidated real estate joint ventures, we include the portion of Annualized Rental Revenue allocable to COPT’s ownership interest. |

(3) | Properties continually owned and 100% operational since at least 1/1/15, excluding properties disposed or held for sale. |

(4) | Newly constructed or redeveloped properties placed in service that were not fully operational by 1/1/15. |

(5) | Includes properties acquired in 2015. |

(6) | Represents total information pertaining to properties owned through an unconsolidated real estate joint venture except for the amounts reported for Annualized Rental Revenue and NOI from real estate operations, which represent the portion allocable to COPT’s ownership interest. See page 34 for additional disclosure regarding this joint venture. |

(7) | The carrying value of operating property assets held for sale as of 9/30/16 totaled $139.7 million. |

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | |||||||||||||||||||||

Consolidated real estate revenues | |||||||||||||||||||||||||||

Defense/IT Locations: | |||||||||||||||||||||||||||

Fort Meade/BW Corridor | $ | 61,460 | $ | 60,912 | $ | 62,509 | $ | 61,683 | $ | 61,400 | $ | 184,881 | $ | 182,591 | |||||||||||||

NoVA Defense/IT | 12,231 | 12,057 | 12,116 | 11,816 | 12,875 | 36,404 | 37,383 | ||||||||||||||||||||

Lackland Air Force Base | 12,532 | 11,651 | 10,225 | 12,233 | 9,018 | 34,408 | 27,426 | ||||||||||||||||||||

Navy Support | 7,232 | 6,998 | 6,934 | 6,840 | 6,886 | 21,164 | 21,337 | ||||||||||||||||||||

Redstone Arsenal | 3,189 | 3,191 | 3,116 | 3,063 | 3,061 | 9,496 | 8,165 | ||||||||||||||||||||

Data Center Shells-Consolidated | 5,175 | 7,288 | 6,330 | 5,930 | 5,665 | 18,793 | 15,816 | ||||||||||||||||||||

Total Defense/IT locations | 101,819 | 102,097 | 101,230 | 101,565 | 98,905 | 305,146 | 292,718 | ||||||||||||||||||||

Regional Office | 20,499 | 23,283 | 23,502 | 25,023 | 26,782 | 67,284 | 73,142 | ||||||||||||||||||||

Wholesale Data Center | 6,809 | 6,804 | 6,493 | 6,099 | 6,078 | 20,106 | 12,933 | ||||||||||||||||||||

Other | 1,827 | 1,740 | 1,862 | 1,790 | 1,921 | 5,429 | 5,798 | ||||||||||||||||||||

Consolidated real estate revenues | $ | 130,954 | $ | 133,924 | $ | 133,087 | $ | 134,477 | $ | 133,686 | $ | 397,965 | $ | 384,591 | |||||||||||||

NOI | |||||||||||||||||||||||||||

Defense/IT Locations: | |||||||||||||||||||||||||||

Fort Meade/BW Corridor | $ | 40,862 | $ | 40,534 | $ | 39,263 | $ | 41,476 | $ | 41,294 | $ | 120,659 | $ | 119,489 | |||||||||||||

NoVA Defense/IT | 7,769 | 7,750 | 7,575 | 7,829 | 7,725 | 23,094 | 21,263 | ||||||||||||||||||||

Lackland Air Force Base | 4,933 | 4,807 | 4,805 | 4,894 | 4,465 | 14,545 | 12,761 | ||||||||||||||||||||

Navy Support | 3,858 | 4,323 | 3,410 | 3,686 | 3,599 | 11,591 | 11,262 | ||||||||||||||||||||

Redstone Arsenal | 2,077 | 2,231 | 2,138 | 2,171 | 2,173 | 6,446 | 5,560 | ||||||||||||||||||||

Data Center Shells | |||||||||||||||||||||||||||

Consolidated properties | 4,647 | 6,462 | 5,520 | 5,358 | 5,133 | 16,629 | 14,090 | ||||||||||||||||||||

COPT’s share of unconsolidated real estate JV (1) | 1,008 | — | — | — | — | 1,008 | — | ||||||||||||||||||||

Total Defense/IT locations | 65,154 | 66,107 | 62,711 | 65,414 | 64,389 | 193,972 | 184,425 | ||||||||||||||||||||

Regional Office | 12,344 | 14,562 | 13,671 | 15,608 | 17,186 | 40,577 | 46,392 | ||||||||||||||||||||

Wholesale Data Center | 3,492 | 4,153 | 3,832 | 4,138 | 2,070 | 11,477 | 4,492 | ||||||||||||||||||||

Other | 1,020 | 961 | 998 | 819 | 1,144 | 2,979 | 3,292 | ||||||||||||||||||||

NOI from real estate operations | $ | 82,010 | $ | 85,783 | $ | 81,212 | $ | 85,979 | $ | 84,789 | $ | 249,005 | $ | 238,601 | |||||||||||||

(1) See page 34 for additional disclosure regarding an unconsolidated real estate joint venture. | |||||||||||||||||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | |||||||||||||||||||||

Cash NOI (1) | |||||||||||||||||||||||||||

Defense/IT Locations: | |||||||||||||||||||||||||||

Fort Meade/BW Corridor | $ | 40,253 | $ | 39,588 | $ | 38,502 | $ | 39,668 | $ | 39,841 | $ | 118,343 | $ | 114,749 | |||||||||||||

NoVA Defense/IT | 7,234 | 7,614 | 7,922 | 8,045 | 6,793 | 22,770 | 17,833 | ||||||||||||||||||||

Lackland Air Force Base | 4,855 | 4,718 | 4,716 | 4,745 | 3,680 | 14,289 | 10,348 | ||||||||||||||||||||

Navy Support | 3,524 | 4,218 | 3,196 | 3,597 | 3,565 | 10,938 | 10,970 | ||||||||||||||||||||

Redstone Arsenal | 2,411 | 2,534 | 2,473 | 2,267 | 1,881 | 7,418 | 5,561 | ||||||||||||||||||||

Data Center Shells | |||||||||||||||||||||||||||

Consolidated properties | 4,549 | 6,077 | 5,108 | 5,024 | 4,802 | 15,734 | 12,742 | ||||||||||||||||||||

COPT’s share of unconsolidated real estate JV (2) | 862 | — | — | — | — | 862 | — | ||||||||||||||||||||

Total Defense/IT locations | 63,688 | 64,749 | 61,917 | 63,346 | 60,562 | 190,354 | 172,203 | ||||||||||||||||||||

Regional Office | 12,480 | 14,152 | 13,000 | 15,031 | 15,943 | 39,632 | 44,179 | ||||||||||||||||||||

Wholesale Data Center | 3,439 | 4,052 | 3,728 | 4,011 | 1,952 | 11,219 | 4,983 | ||||||||||||||||||||

Other | 935 | 892 | 823 | 835 | 1,117 | 2,650 | 3,222 | ||||||||||||||||||||

Cash NOI from real estate operations (1) | $ | 80,542 | $ | 83,845 | $ | 79,468 | $ | 83,223 | $ | 79,574 | $ | 243,855 | $ | 224,587 | |||||||||||||

Straight line rent adjustments and lease incentive amortization | (1,086 | ) | (897 | ) | 546 | 2,254 | 5,217 | (1,437 | ) | 9,604 | |||||||||||||||||

Add: Amortization of deferred market rental revenue | (201 | ) | (189 | ) | (190 | ) | (178 | ) | (293 | ) | (580 | ) | (542 | ) | |||||||||||||

Less: Amortization of below-market cost arrangements | (241 | ) | (241 | ) | (240 | ) | (284 | ) | (289 | ) | (722 | ) | (805 | ) | |||||||||||||

Add: Lease termination fee, gross | 471 | 417 | 980 | 417 | 190 | 1,868 | 1,956 | ||||||||||||||||||||

Add: Cash NOI on tenant funded landlord assets | 2,379 | 2,848 | 648 | 547 | 390 | 5,875 | 3,801 | ||||||||||||||||||||

Cash NOI adjustments in unconsolidated real estate JV | 146 | — | — | — | — | 146 | — | ||||||||||||||||||||

NOI from real estate operations | $ | 82,010 | $ | 85,783 | $ | 81,212 | $ | 85,979 | $ | 84,789 | $ | 249,005 | $ | 238,601 | |||||||||||||

(1) | Effective in the current quarter, we changed our definition of Cash NOI used for the above segment presentation to exclude the effects of gross lease termination fees and revenue recognized as a result of tenant-funded landlord assets. As a result of this change, our definition is consistent with the definition of Cash NOI used for our Same Office Property presentation. |

(2) | See page 34 for additional disclosure regarding an unconsolidated real estate joint venture. |

Number of Buildings | Rentable Square Feet | Three Months Ended | Nine Months Ended | |||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | ||||||||||||||||||||

Core Portfolio: | ||||||||||||||||||||||||||

Defense/IT Locations: | ||||||||||||||||||||||||||

Fort Meade/BW Corridor | 78 | 7,425 | 95.0 | % | 94.9 | % | 95.0 | % | 96.6 | % | 96.0 | % | 95.0 | % | 95.5 | % | ||||||||||

NoVA Defense/IT | 9 | 1,203 | 76.4 | % | 74.1 | % | 74.5 | % | 75.9 | % | 75.4 | % | 75.0 | % | 75.9 | % | ||||||||||

Lackland Air Force Base | 6 | 792 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||||

Navy Support | 20 | 1,233 | 75.2 | % | 74.6 | % | 74.0 | % | 73.9 | % | 73.3 | % | 74.6 | % | 77.7 | % | ||||||||||

Redstone Arsenal | 5 | 563 | 99.4 | % | 98.8 | % | 97.5 | % | 95.7 | % | 94.5 | % | 98.6 | % | 89.5 | % | ||||||||||

Data Center Shells | 3 | 451 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||||

Total Defense/IT Locations | 121 | 11,667 | 91.7 | % | 91.4 | % | 91.3 | % | 92.4 | % | 91.8 | % | 91.5 | % | 91.8 | % | ||||||||||

Regional Office | 5 | 1,088 | 98.2 | % | 98.8 | % | 97.5 | % | 96.0 | % | 95.1 | % | 98.2 | % | 94.4 | % | ||||||||||

Core Portfolio Same Office Properties | 126 | 12,755 | 92.3 | % | 92.0 | % | 91.8 | % | 92.7 | % | 92.1 | % | 92.0 | % | 92.0 | % | ||||||||||

Other Same Office Properties | 3 | 286 | 44.0 | % | 43.5 | % | 43.5 | % | 44.2 | % | 43.8 | % | 43.7 | % | 45.3 | % | ||||||||||

Total Same Office Properties | 129 | 13,041 | 91.2 | % | 90.9 | % | 90.8 | % | 91.6 | % | 91.1 | % | 91.0 | % | 91.0 | % | ||||||||||

Corporate Office Properties Trust Same Office Properties (1) Period End Occupancy Rates by Segment (square feet in thousands) | ||||||||||||||||||||||||||

Number of Buildings | Rentable Square Feet | |||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | ||||||||||||||||||||||

Core Portfolio: | ||||||||||||||||||||||||||

Defense/IT Locations: | ||||||||||||||||||||||||||

Fort Meade/BW Corridor | 78 | 7,425 | 95.1 | % | 94.8 | % | 94.8 | % | 96.5 | % | 96.3 | % | ||||||||||||||

NoVA Defense/IT | 9 | 1,203 | 78.1 | % | 73.9 | % | 74.5 | % | 75.8 | % | 76.1 | % | ||||||||||||||

Lackland Air Force Base | 6 | 792 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||||||||

Navy Support | 20 | 1,233 | 75.3 | % | 76.4 | % | 73.4 | % | 73.8 | % | 73.1 | % | ||||||||||||||

Redstone Arsenal | 5 | 563 | 100.0 | % | 98.8 | % | 98.8 | % | 96.7 | % | 95.2 | % | ||||||||||||||

Data Center Shells | 3 | 451 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | ||||||||||||||

Total Defense/IT Locations | 121 | 11,667 | 92.0 | % | 91.5 | % | 91.2 | % | 92.4 | % | 92.1 | % | ||||||||||||||

Regional Office | 5 | 1,088 | 97.8 | % | 99.3 | % | 98.0 | % | 96.3 | % | 95.2 | % | ||||||||||||||

Core Portfolio Same Office Properties | 126 | 12,755 | 92.5 | % | 92.1 | % | 91.8 | % | 92.7 | % | 92.3 | % | ||||||||||||||

Other Same Office Properties | 3 | 286 | 44.0 | % | 43.5 | % | 43.5 | % | 44.4 | % | 43.8 | % | ||||||||||||||

Total Same Office Properties | 129 | 13,041 | 91.4 | % | 91.1 | % | 90.7 | % | 91.6 | % | 91.3 | % | ||||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | |||||||||||||||||||||

Same office property real estate revenues | |||||||||||||||||||||||||||

Defense/IT Locations: | |||||||||||||||||||||||||||

Fort Meade/BW Corridor | $ | 57,675 | $ | 57,011 | $ | 58,918 | $ | 58,128 | $ | 57,879 | $ | 173,604 | $ | 172,757 | |||||||||||||

NoVA Defense/IT | 6,650 | 6,500 | 6,755 | 6,666 | 6,668 | 19,905 | 20,210 | ||||||||||||||||||||

Lackland Air Force Base | 10,536 | 10,031 | 8,699 | 10,564 | 7,912 | 29,266 | 24,889 | ||||||||||||||||||||

Navy Support | 7,232 | 6,998 | 6,934 | 6,840 | 6,887 | 21,164 | 21,337 | ||||||||||||||||||||

Redstone Arsenal | 2,828 | 2,847 | 2,771 | 2,718 | 2,716 | 8,446 | 7,669 | ||||||||||||||||||||

Data Center Shells | 3,050 | 3,095 | 3,040 | 3,051 | 3,081 | 9,185 | 9,189 | ||||||||||||||||||||

Total Defense/IT Locations | 87,971 | 86,482 | 87,117 | 87,967 | 85,143 | 261,570 | 256,051 | ||||||||||||||||||||

Regional Office | 9,402 | 9,379 | 9,158 | 8,954 | 9,550 | 27,939 | 27,805 | ||||||||||||||||||||

Other Properties | 1,016 | 951 | 930 | 965 | 1,072 | 2,897 | 3,082 | ||||||||||||||||||||

Same office property real estate revenues | $ | 98,389 | $ | 96,812 | $ | 97,205 | $ | 97,886 | $ | 95,765 | $ | 292,406 | $ | 286,938 | |||||||||||||

Same office property NOI | |||||||||||||||||||||||||||

Defense/IT Locations: | |||||||||||||||||||||||||||

Fort Meade/BW Corridor | $ | 38,416 | $ | 38,097 | $ | 37,396 | $ | 39,117 | $ | 38,958 | $ | 113,909 | $ | 113,519 | |||||||||||||

NoVA Defense/IT | 4,119 | 3,969 | 4,000 | 4,158 | 4,093 | 12,088 | 12,040 | ||||||||||||||||||||

Lackland Air Force Base | 3,741 | 3,746 | 3,749 | 3,746 | 3,672 | 11,236 | 11,063 | ||||||||||||||||||||

Navy Support | 3,875 | 4,340 | 3,435 | 3,706 | 3,605 | 11,650 | 11,268 | ||||||||||||||||||||

Redstone Arsenal | 1,961 | 1,981 | 1,872 | 1,905 | 1,872 | 5,814 | 5,122 | ||||||||||||||||||||

Data Center Shells | 2,758 | 2,764 | 2,769 | 2,770 | 2,771 | 8,291 | 8,307 | ||||||||||||||||||||

Total Defense/IT Locations | 54,870 | 54,897 | 53,221 | 55,402 | 54,971 | 162,988 | 161,319 | ||||||||||||||||||||

Regional Office | 5,819 | 5,790 | 5,571 | 5,509 | 5,976 | 17,180 | 16,815 | ||||||||||||||||||||

Other Properties | 606 | 577 | 488 | 411 | 642 | 1,671 | 1,619 | ||||||||||||||||||||

Same office property NOI | $ | 61,295 | $ | 61,264 | $ | 59,280 | $ | 61,322 | $ | 61,589 | $ | 181,839 | $ | 179,753 | |||||||||||||

Three Months Ended | Nine Months Ended | ||||||||||||||||||||||||||

9/30/16 | 6/30/16 | 3/31/16 | 12/31/15 | 9/30/15 | 9/30/16 | 9/30/15 | |||||||||||||||||||||

Same office property cash NOI | |||||||||||||||||||||||||||

Defense/IT Locations: | |||||||||||||||||||||||||||

Fort Meade/BW Corridor | $ | 38,322 | $ | 37,907 | $ | 37,114 | $ | 38,222 | $ | 38,245 | $ | 113,343 | $ | 109,825 | |||||||||||||

NoVA Defense/IT | 3,340 | 3,545 | 3,999 | 4,138 | 3,971 | 10,884 | 11,588 | ||||||||||||||||||||

Lackland Air Force Base | 3,742 | 3,748 | 3,751 | 3,748 | 3,574 | 11,241 | 10,768 | ||||||||||||||||||||

Navy Support | 3,542 | 4,234 | 3,221 | 3,617 | 3,570 | 10,997 | 10,975 | ||||||||||||||||||||

Redstone Arsenal | 2,312 | 2,307 | 2,229 | 2,118 | 1,887 | 6,848 | 5,526 | ||||||||||||||||||||

Data Center Shells | 2,915 | 2,890 | 2,883 | 2,877 | 2,865 | 8,688 | 8,514 | ||||||||||||||||||||

Total Defense/IT Locations | 54,173 | 54,631 | 53,197 | 54,720 | 54,112 | 162,001 | 157,196 | ||||||||||||||||||||

Regional Office | 6,218 | 6,252 | 6,042 | 5,801 | 5,547 | 18,512 | 16,113 | ||||||||||||||||||||

Other Properties | 561 | 554 | 470 | 407 | 638 | 1,585 | 1,633 | ||||||||||||||||||||

Same office property cash NOI | $ | 60,952 | $ | 61,437 | $ | 59,709 | $ | 60,928 | $ | 60,297 | $ | 182,098 | $ | 174,942 | |||||||||||||

Straight line rent adjustments and lease incentive amortization | (2,230 | ) | (3,172 | ) | (1,761 | ) | (338 | ) | 965 | (7,163 | ) | 3,175 | |||||||||||||||

Add: Amortization of deferred market rental revenue | 22 | 34 | 34 | 28 | 16 | 90 | 71 | ||||||||||||||||||||

Less: Amortization of below-market cost arrangements | (218 | ) | (219 | ) | (218 | ) | (259 | ) | (264 | ) | (655 | ) | (775 | ) | |||||||||||||

Add: Lease termination fee, gross | 390 | 336 | 953 | 416 | 185 | 1,679 | 1,950 | ||||||||||||||||||||

Add: Cash NOI on tenant-funded landlord assets | 2,379 | 2,848 | 563 | 547 | 390 | 5,790 | 390 | ||||||||||||||||||||

Same office property NOI | $ | 61,295 | $ | 61,264 | $ | 59,280 | $ | 61,322 | $ | 61,589 | $ | 181,839 | $ | 179,753 | |||||||||||||

Percentage change in same office property cash NOI (1) | 1.1 | % | 4.1 | % | |||||||||||||||||||||||

(1) | Represents the change between the current period and the same period in the prior year. |

Ft Meade/BW Corridor | NoVA Defense/IT | Navy Support | Regional Office | Total Office | |||||||||||||||

Renewed Space | |||||||||||||||||||

Leased Square Feet | 79 | 213 | 71 | 234 | 597 | ||||||||||||||

Expiring Square Feet | 120 | 213 | 85 | 302 | 720 | ||||||||||||||

Vacating Square Feet | 41 | — | 13 | 68 | 123 | ||||||||||||||

Retention Rate (% based upon square feet) | 65.6 | % | 100.0 | % | 84.4 | % | 77.4 | % | 82.9 | % | |||||||||

Statistics for Completed Leasing: | |||||||||||||||||||

Average Committed Cost per Square Foot | $ | 27.86 | $ | 14.86 | $ | 11.21 | $ | 71.58 | $ | 38.36 | |||||||||

Weighted Average Lease Term in Years | 5.9 | 7.0 | 3.7 | 9.9 | 7.6 | ||||||||||||||

GAAP Rent Per Square Foot | |||||||||||||||||||

Renewal GAAP Rent | $ | 29.37 | $ | 32.10 | $ | 28.31 | $ | 35.51 | $ | 32.62 | |||||||||

Expiring GAAP Rent | $ | 28.06 | $ | 30.84 | $ | 30.76 | $ | 38.18 | $ | 33.34 | |||||||||

Change in GAAP Rent | 4.7 | % | 4.1 | % | (8.0 | )% | (7.0 | )% | (2.2 | )% | |||||||||

Cash Rent Per Square Foot | |||||||||||||||||||

Renewal Cash Rent | $ | 29.11 | $ | 31.22 | $ | 28.26 | $ | 35.36 | $ | 32.21 | |||||||||

Expiring Cash Rent | $ | 30.46 | $ | 32.78 | $ | 32.11 | $ | 43.36 | $ | 36.54 | |||||||||

Change in Cash Rent | (4.4 | )% | (4.8 | )% | (12.0 | )% | (18.5 | )% | (11.9 | )% | |||||||||

Average escalations per year | 2.5 | % | 2.3 | % | 2.1 | % | 2.3 | % | 2.3 | % | |||||||||

New Leases | |||||||||||||||||||

Development and Redevelopment Space | |||||||||||||||||||

Leased Square Feet | 19 | 7 | — | — | 26 | ||||||||||||||

Statistics for Completed Leasing: | |||||||||||||||||||

Average Committed Cost per Square Foot | $ | 71.64 | $ | 100.40 | $ | — | $ | — | $ | 79.36 | |||||||||

Weighted Average Lease Term in Years | 8.5 | 11.4 | — | — | 9.3 | ||||||||||||||

GAAP Rent Per Square Foot | $ | 28.43 | $ | 32.11 | $ | — | $ | — | $ | 29.42 | |||||||||

Cash Rent Per Square Foot | $ | 25.56 | $ | 30.73 | $ | — | $ | — | $ | 26.95 | |||||||||

Other New Leases (2) | |||||||||||||||||||

Leased Square Feet | 25 | 12 | 56 | 25 | 118 | ||||||||||||||

Statistics for Completed Leasing: | |||||||||||||||||||

Average Committed Cost per Square Foot | $ | 39.65 | $ | 74.35 | $ | 57.92 | $ | 40.87 | $ | 51.98 | |||||||||

Weighted Average Lease Term in Years | 5.4 | 7.4 | 6.9 | 6.3 | 6.5 | ||||||||||||||

GAAP Rent Per Square Foot | $ | 25.28 | $ | 28.16 | $ | 33.80 | $ | 28.47 | $ | 30.30 | |||||||||

Cash Rent Per Square Foot | $ | 25.11 | $ | 27.66 | $ | 37.20 | $ | 28.40 | $ | 31.81 | |||||||||

Total Square Feet Leased | 123 | 231 | 128 | 259 | 741 | ||||||||||||||

Average escalations per year | 2.7 | % | 2.3 | % | 1.0 | % | 2.3 | % | 2.2 | % | |||||||||

(1) | Activity is exclusive of owner occupied space and leases with less than a one-year term. Weighted average lease term was calculated assuming no exercise of any existing early termination rights. Committed costs for leasing are reported above in the period of lease execution. Actual capital expenditures for leasing are reported on page 9 in the period such costs are incurred. |

Ft Meade/BW Corridor | NoVA Defense/IT | Navy Support | Redstone Arsenal | Data Center Shells | Regional Office | Other | Total Office | ||||||||||||||||||||||||

Renewed Space | |||||||||||||||||||||||||||||||

Leased Square Feet | 652 | 295 | 120 | 1 | — | 263 | 23 | 1,353 | |||||||||||||||||||||||

Expiring Square Feet | 874 | 351 | 134 | 1 | — | 332 | 32 | 1,725 | |||||||||||||||||||||||

Vacating Square Feet | 222 | 56 | 14 | — | — | 69 | 10 | 371 | |||||||||||||||||||||||

Retention Rate (% based upon square feet) | 74.6 | % | 84.0 | % | 89.3 | % | 100.0 | % | — | % | 79.2 | % | 70.1 | % | 78.5 | % | |||||||||||||||

Statistics for Completed Leasing: | |||||||||||||||||||||||||||||||

Average Committed Cost per Square Foot | $ | 12.30 | $ | 11.37 | $ | 10.52 | $ | 6.14 | $ | — | $ | 67.92 | $ | — | $ | 22.52 | |||||||||||||||

Weighted Average Lease Term in Years | 5.6 | 5.6 | 3.1 | 0.5 | — | 9.4 | 1.0 | 6.0 | |||||||||||||||||||||||

GAAP Rent Per Square Foot | |||||||||||||||||||||||||||||||

Renewal GAAP Rent | $ | 33.90 | $ | 31.41 | $ | 27.23 | $ | 27.08 | $ | — | $ | 35.04 | $ | 22.85 | $ | 32.80 | |||||||||||||||

Expiring GAAP Rent | $ | 30.59 | $ | 29.68 | $ | 29.77 | $ | 26.55 | $ | — | $ | 37.04 | $ | 20.79 | $ | 31.40 | |||||||||||||||

Change in GAAP Rent | 10.8 | % | 5.9 | % | (8.5 | )% | 2.0 | % | — | % | (5.4 | )% | 9.9 | % | 4.5 | % | |||||||||||||||

Cash Rent Per Square Foot | |||||||||||||||||||||||||||||||

Renewal Cash Rent | $ | 32.43 | $ | 30.30 | $ | 27.18 | $ | 25.50 | $ | — | $ | 34.76 | $ | 22.85 | $ | 31.78 | |||||||||||||||

Expiring Cash Rent | $ | 32.50 | $ | 31.25 | $ | 30.79 | $ | 25.00 | $ | — | $ | 41.75 | $ | 22.85 | $ | 33.70 | |||||||||||||||

Change in Cash Rent | (0.2 | )% | (3.0 | )% | (11.7 | )% | 2.0 | % | — | % | (16.7 | )% | — | % | (5.7 | )% | |||||||||||||||

Average escalations per year | 2.8 | % | 2.3 | % | 2.1 | % | — | % | — | % | 2.3 | % | — | % | 2.5 | % | |||||||||||||||

New Leases | |||||||||||||||||||||||||||||||

Development and Redevelopment Space | |||||||||||||||||||||||||||||||

Leased Square Feet | 23 | 35 | — | — | 513 | — | — | 571 | |||||||||||||||||||||||

Statistics for Completed Leasing: | |||||||||||||||||||||||||||||||

Average Committed Cost per Square Foot | $ | 64.53 | $ | 89.01 | $ | — | $ | — | $ | — | $ | — | $ | — | $ | 8.10 | |||||||||||||||

Weighted Average Lease Term in Years | 7.3 | 10.2 | — | — | 10.0 | — | — | 9.9 | |||||||||||||||||||||||

GAAP Rent Per Square Foot | $ | 28.43 | $ | 34.24 | $ | — | $ | — | $ | 13.57 | $ | — | $ | — | $ | 15.44 | |||||||||||||||

Cash Rent Per Square Foot | $ | 26.02 | $ | 32.58 | $ | — | $ | — | $ | 12.45 | $ | — | $ | — | $ | 14.24 | |||||||||||||||

Other New Leases (2) | |||||||||||||||||||||||||||||||

Leased Square Feet | 173 | 50 | 89 | 7 | — | 42 | 6 | 367 | |||||||||||||||||||||||

Statistics for Completed Leasing: | |||||||||||||||||||||||||||||||

Average Committed Cost per Square Foot | $ | 34.81 | $ | 58.90 | $ | 47.65 | $ | 56.66 | $ | — | $ | 40.75 | $ | 36.57 | $ | 42.31 | |||||||||||||||

Weighted Average Lease Term in Years | 6.6 | 6.2 | 5.6 | 6.2 | — | 7.4 | 3.8 | 6.3 | |||||||||||||||||||||||

GAAP Rent Per Square Foot | $ | 28.74 | $ | 26.24 | $ | 32.05 | $ | 25.18 | $ | — | $ | 28.88 | $ | 21.09 | $ | 29.01 | |||||||||||||||

Cash Rent Per Square Foot | $ | 27.95 | $ | 25.86 | $ | 34.29 | $ | 23.40 | $ | — | $ | 28.15 | $ | 20.49 | $ | 29.00 | |||||||||||||||

Total Square Feet Leased | 848 | 380 | 209 | 8 | 513 | 304 | 29 | 2,292 | |||||||||||||||||||||||

Average escalations per year | 2.8 | % | 2.4 | % | 1.3 | % | 2.8 | % | 2.3 | % | 2.3 | % | 1.6 | % | 2.4 | % | |||||||||||||||

Average escalations excl. data center shells | 2.5 | % | |||||||||||||||||||||||||||||

(1) | Activity is exclusive of owner occupied space and leases with less than a one-year term. Weighted average lease term was calculated assuming no exercise of any existing early termination rights. Committed costs for leasing are reported above in the period of lease execution. Actual capital expenditures for leasing are reported on page 9 in the period such costs are incurred. |

Year and Region of Lease (2) | Number of Leases Expiring | Square Footage of Leases Expiring | Annual Rental Revenue of Expiring Leases (3) | Percentage of Total Annualized Rental Revenue Expiring (3) | Annual Rental Revenue of Expiring Leases per Occupied Square Foot | ||||||||||||

Core Portfolio | |||||||||||||||||

Ft Meade/BW Corridor | 14 | 283 | $ | 9,926 | 2.2 | % | $35.12 | ||||||||||

NoVA Defense/IT | 5 | 35 | 654 | 0.1 | % | 18.48 | |||||||||||

Navy Support | 4 | 57 | 1,048 | 0.2 | % | 18.27 | |||||||||||

Regional Office | 10 | 96 | 3,426 | 0.8 | % | 35.70 | |||||||||||

2016 | 33 | 471 | 15,054 | 3.4 | % | 31.94 | |||||||||||

Ft Meade/BW Corridor | 38 | 1,164 | 37,615 | 8.5 | % | 32.33 | |||||||||||

NoVA Defense/IT | 3 | 28 | 1,118 | 0.3 | % | 39.45 | |||||||||||

Navy Support | 16 | 135 | 2,760 | 0.6 | % | 20.37 | |||||||||||

Redstone Arsenal | 1 | 2 | 34 | — | % | 19.89 | |||||||||||

Regional Office | 11 | 114 | 3,949 | 0.9 | % | 34.59 | |||||||||||

2017 | 69 | 1,443 | 45,476 | 10.3 | % | 31.51 | |||||||||||

Ft Meade/BW Corridor | 44 | 985 | 33,160 | 7.5 | % | 33.67 | |||||||||||

NoVA Defense/IT | 5 | 206 | 7,630 | 1.7 | % | 37.11 | |||||||||||

Navy Support | 17 | 181 | 5,320 | 1.2 | % | 29.47 | |||||||||||

Redstone Arsenal | 3 | 251 | 6,478 | 1.5 | % | 25.78 | |||||||||||

Data Center Shells-Consolidated properties | 1 | 155 | 2,498 | 0.6 | % | 16.11 | |||||||||||

Regional Office | 9 | 126 | 4,049 | 0.9 | % | 32.21 | |||||||||||

2018 | 79 | 1,904 | 59,135 | 13.4 | % | 31.07 | |||||||||||

Ft Meade/BW Corridor | 43 | 1,477 | 48,097 | 10.9 | % | 32.56 | |||||||||||

NoVA Defense/IT | 6 | 258 | 9,798 | 2.2 | % | 37.99 | |||||||||||

Navy Support | 10 | 59 | 1,596 | 0.4 | % | 26.88 | |||||||||||

Redstone Arsenal | 4 | 71 | 1,465 | 0.3 | % | 20.63 | |||||||||||

Regional Office | 11 | 169 | 4,637 | 1.0 | % | 27.39 | |||||||||||

2019 | 74 | 2,034 | 65,593 | 14.8 | % | 32.24 | |||||||||||

Ft Meade/BW Corridor | 38 | 1,049 | 34,135 | 7.7 | % | 32.54 | |||||||||||

NoVA Defense/IT | 4 | 121 | 3,272 | 0.7 | % | 26.94 | |||||||||||

Lackland Air Force Base | 2 | 250 | 9,092 | 2.1 | % | 36.32 | |||||||||||

Navy Support | 17 | 175 | 7,012 | 1.6 | % | 40.14 | |||||||||||

Redstone Arsenal | 3 | 141 | 2,984 | 0.7 | % | 21.22 | |||||||||||

Regional Office | 11 | 67 | 2,017 | 0.5 | % | 29.96 | |||||||||||

2020 | 75 | 1,803 | 58,512 | 13.2 | % | 32.45 | |||||||||||

Thereafter | |||||||||||||||||

Consolidated Properties | 172 | 6,199 | 193,657 | 43.7 | % | 28.51 | |||||||||||

Unconsolidated JV Properties | 6 | 962 | 5,233 | 1.2 | % | 10.88 | |||||||||||

Core Portfolio | 508 | 14,816 | $ | 442,660 | 100.0 | % | $29.88 | ||||||||||

Year and Region of Lease (2) | Number of Leases Expiring | Square Footage of Leases Expiring | Annual Rental Revenue of Expiring Leases (3) | Percentage of Total Annualized Rental Revenue Expiring (3) | Annual Rental Revenue of Expiring Leases per Occupied Square Foot | ||||||||||||

Core Portfolio | 508 | 14,816 | $ | 442,660 | 100.0 | % | $29.88 | ||||||||||

Office Properties Held for Sale and Other | |||||||||||||||||

Ft Meade/BW Corridor | 19 | 231 | 5,095 | 17.6 | % | 22.05 | |||||||||||

NoVA Defense/IT | 14 | 306 | 8,559 | 29.6 | % | 27.94 | |||||||||||

Regional Office | 27 | 353 | 8,371 | 29.0 | % | 23.71 | |||||||||||

Other | 16 | 263 | 6,872 | 23.8 | % | 26.12 | |||||||||||

Office Properties Held for Sale and Other Total Average | 76 | 1,153 | 28,897 | 100.0 | % | 25.05 | |||||||||||

Total Portfolio | 584 | $ | 15,969 | $ | 471,557 | $29.53 | |||||||||||

Consolidated Portfolio | 578 | 15,007 | $ | 466,324 | |||||||||||||

Unconsolidated JV Properties | 6 | 962 | $ | 5,233 | |||||||||||||

Year of Lease Expiration | Number of Leases Expiring | Raised Floor Square Footage | Critical Load(MW) | Total Annual Rental Revenue of Expiring Leases (3)(000's) | ||||

2017 | 1 | 9 | 2.00 | $ | 2,280 | |||

2018 | 2 | 1 | 0.26 | 536 | ||||

2019 | 1 | 6 | 1.00 | 2,274 | ||||

2020 | 2 | 19 | 11.45 | 13,871 | ||||

2022 | 1 | 6 | 1.00 | 1,559 | ||||

15.71 | $ | 20,519 | ||||||

(1) | This expiration analysis reflects occupied space of our total portfolio (including consolidated and unconsolidated properties) and includes the effect of early renewals completed on existing leases but excludes the effect of new tenant leases on square feet yet to commence as of September 30, 2016 of 266,000 for the portfolio, including 232,000 for the Core Portfolio. With regard to properties owned through unconsolidated real estate joint ventures, the amounts reported above reflect 100% of the properties’ square footage but only reflect the portion of Annualized Rental Revenue that was allocable to COPT’s ownership interest. |

(2) | A number of our leases are subject to certain early termination provisions. The year of lease expiration was computed assuming no exercise of such early termination rights. |

(3) | Total Annualized Rental Revenue is the monthly contractual base rent as of September 30, 2016 multiplied by 12 plus the estimated annualized expense reimbursements under existing leases. The amounts reported above for Annualized Rental Revenue include the portion of properties owned through an unconsolidated real estate joint venture that was allocable to COPT’s ownership interest. |

Tenant | Number of Leases | Total Occupied Square Feet | Percentage of Total Occupied Square Feet | Total Annualized Rental Revenue (2) | Percentage of Total Annualized Rental Revenue (2) | Weighted Average Remaining Lease Term (3) | |||||||||||||

United States Government | (4) | 61 | 3,760 | 23.5 | % | $ | 141,192 | 29.9 | % | 4.7 | |||||||||

Northrop Grumman Corporation | 8 | 757 | 4.7 | % | 22,509 | 4.8 | % | 3.7 | |||||||||||

The Boeing Company | 11 | 685 | 4.3 | % | 20,204 | 4.3 | % | 2.8 | |||||||||||

General Dynamics Corporation | 7 | 528 | 3.3 | % | 19,536 | 4.1 | % | 4.8 | |||||||||||

Vadata Inc. | (1) | 9 | 1,408 | 8.8 | % | 12,040 | 2.6 | % | 8.6 | ||||||||||

Computer Sciences Corporation | 3 | 279 | 1.7 | % | 10,811 | 2.3 | % | 2.4 | |||||||||||

CareFirst, Inc. | 2 | 300 | 1.9 | % | 10,422 | 2.2 | % | 6.4 | |||||||||||

Booz Allen Hamilton, Inc. | 6 | 294 | 1.8 | % | 9,994 | 2.1 | % | 4.5 | |||||||||||

Wells Fargo & Company | 3 | 190 | 1.2 | % | 8,353 | 1.8 | % | 10.8 | |||||||||||

CACI Technologies, Inc. | 3 | 225 | 1.4 | % | 7,285 | 1.5 | % | 4.0 | |||||||||||

AT&T Corporation | 3 | 308 | 1.9 | % | 6,019 | 1.3 | % | 2.6 | |||||||||||

The Raytheon Company | 6 | 168 | 1.1 | % | 5,967 | 1.3 | % | 2.4 | |||||||||||

KEYW Corporation | 2 | 211 | 1.3 | % | 5,895 | 1.3 | % | 7.2 | |||||||||||

Science Applications International Corp. | 4 | 146 | 0.9 | % | 5,122 | 1.1 | % | 4.2 | |||||||||||

Miles & Stockbridge, PC | 2 | 156 | 1.0 | % | 5,052 | 1.1 | % | 11.0 | |||||||||||

Transamerica Life Insurance Company | 2 | 159 | 1.0 | % | 4,815 | 1.0 | % | 5.2 | |||||||||||

Harris Corporation | 6 | 170 | 1.1 | % | 4,710 | 1.0 | % | 5.5 | |||||||||||

University of Maryland | 3 | 172 | 1.1 | % | 4,692 | 1.0 | % | 4.8 | |||||||||||

Kratos Defense and Security Solutions | 1 | 131 | 0.8 | % | 4,638 | 1.0 | % | 3.6 | |||||||||||

The Mitre Corporation | 4 | 122 | 0.8 | % | 4,267 | 0.9 | % | 3.2 | |||||||||||

Subtotal Top 20 Office Tenants | 146 | 10,168 | 63.7 | % | 313,523 | 66.5 | % | 5.2 | |||||||||||

All remaining tenants | 438 | 5,801 | 36.3 | % | 158,034 | 33.5 | % | 4.2 | |||||||||||

Total/Weighted Average | 584 | 15,969 | 100.0 | % | $ | 471,557 | 100.0 | % | 4.8 | ||||||||||

Property Segment/Subsegment | Business Park/Submarket | Number of Buildings | Square Feet | Transaction Date | Occupancy on Transaction Date | Transaction Price | |||||||||||||

Quarter Ended 3/31/16 | |||||||||||||||||||

Colorado Springs Land | N/A | N/A | N/A | N/A | Various | N/A | $ | 5,701 | |||||||||||

Quarter Ended 9/30/16 | |||||||||||||||||||

50% interest in DC8, 9, 10, 11, 12 and 14 | Data Center Shells | Ashburn and Prince William County | 6 | 962 | 7/21/2016 | 100.0% | 73,821 | (1) | |||||||||||

Arborcrest Corporate Campus properties | Regional Office | Greater Philadelphia | 4 | 654 | 8/4/2016 | 100.0% | 142,800 | ||||||||||||

8003 Corporate Drive | Regional Office | White Marsh | 1 | 18 | 8/17/2016 | 100.0% | 2,400 | ||||||||||||

1341 and 1343 Ashton Road | Fort Meade/BW Corridor | BWI South | 2 | 25 | 9/9/2016 | 60.7% | 2,900 | ||||||||||||

8007, 8013, 8015, 8019 and 8023-8027 Corporate Drive | Regional Office | White Marsh | 5 | 130 | 9/21/2016 | 77.8% | 14,513 | ||||||||||||

1302, 1304 and 1306 Concourse Drive | Fort Meade/BW Corridor | Airport Square | 3 | 299 | 9/29/2016 | 83.1% | 48,100 | ||||||||||||

Subtotal - Quarter Ended 9/30/16 | 21 | 2,088 | 284,534 | ||||||||||||||||

Subsequent to 9/30/16 (through 10/26/16) | |||||||||||||||||||

2900 Towerview Road | NoVA Defense/IT | Route 28 South | 1 | 151 | 10/19/2016 | 100.0% | 12,100 | ||||||||||||

Colorado Springs Land | N/A | N/A | N/A | N/A | 10/26/2016 | N/A | 2,000 | ||||||||||||

Subtotal - Subsequent to 9/30/16 (through 10/26/16) | 1 | 151 | 14,100 | ||||||||||||||||

Year to Date Dispositions through 10/26/16 | 22 | 2,239 | $ | 304,335 | |||||||||||||||

Construction Projects (1) | Redevelopment Projects (2) | Land Owned/Controlled (3) | Total | ||||||||||||

Segment | Rentable Square Feet | ||||||||||||||

Defense/IT Locations: | |||||||||||||||

Fort Meade/BW Corridor | 336 | 104 | 4,175 | 4,615 | |||||||||||

NoVA Defense/IT | 401 | — | 1,614 | 2,015 | |||||||||||

Lackland Air Force Base | — | — | 1,033 | 1,033 | |||||||||||

Navy Support | — | — | 109 | 109 | |||||||||||

Redstone Arsenal | 19 | — | 4,084 | 4,103 | |||||||||||

Data Center Shells | 365 | — | 422 | 787 | |||||||||||

Subtotal Defense/IT Locations | 1,121 | 104 | 11,437 | 12,662 | |||||||||||

Regional Office | — | — | 1,089 | 1,089 | |||||||||||

Other | — | — | 1,578 | 1,578 | |||||||||||

Total | 1,121 | 104 | 14,104 | 15,329 | |||||||||||

Costs to date by region | |||||||||||||||

Defense/IT Locations: | |||||||||||||||

Fort Meade/BW Corridor | $ | 62,889 | $ | 20,346 | $ | 133,997 | $ | 217,232 | |||||||

NoVA Defense/IT | 44,072 | — | 92,890 | 136,962 | |||||||||||

Lackland Air Force Base | — | — | 20,197 | 20,197 | |||||||||||

Navy Support | — | — | 2,590 | 2,590 | |||||||||||

Redstone Arsenal | 4,578 | — | 18,417 | 22,995 | |||||||||||

Data Center Shells | 23,475 | — | 9,838 | 33,313 | |||||||||||

Subtotal Defense/IT Locations | 135,014 | 20,346 | 277,929 | 433,289 | |||||||||||

Regional Office | — | — | 64,591 | 64,591 | |||||||||||

Other | — | — | 29,319 | 29,319 | |||||||||||

Total | $ | 135,014 | $ | 20,346 | $ | 371,839 | $ | 527,199 | |||||||

Reconciliation to amounts included in projects in development or held for future development, including land costs, as reported on consolidated balance sheet | |||||||||||||||

Operating properties | (73,779 | ) | (6,216 | ) | (25,833 | ) | (105,828 | ) | |||||||

Assets held for sale | — | — | (21,780 | ) | (21,780 | ) | |||||||||

Deferred leasing costs and other assets | (3,017 | ) | (305 | ) | — | (3,322 | ) | ||||||||

Projects in development or held for future development, including associated land costs (4) | $ | 58,218 | $ | 13,825 | $ | 324,226 | $ | 396,269 | |||||||

(1) | Represents construction projects as listed on page 25. |

(2) | Represents redevelopment projects as listed on page 26. |

(3) | Represents our land owned/controlled as listed on page 28. |

(4) | Represents total of costs included in lines on our consolidated balance sheet entitled “construction and redevelopment in progress, including land” and “land owned/controlled”. |

Property Segment | Park/Submarket | Total Rentable Square Feet | Percentage Leased as of 9/30/16 | as of 9/30/16 (2) | Actual or Anticipated Shell Completion Date | Anticipated Operational Date (3) | ||||||||||||

Anticipated Total Cost | Cost to Date | Cost to Date Placed in Service | ||||||||||||||||

Property and Location | ||||||||||||||||||

Under Construction | ||||||||||||||||||

Bethlehem Technology Park - DC19 Manassas, Virginia | Data Center Shells | Manassas | 149 | 100% | 21,608 | 16,468 | — | 4Q 16 | 4Q 16 | |||||||||

Bethlehem Technology Park - DC20 Manassas, Virginia | Data Center Shells | Manassas | 216 | 100% | 29,913 | 7,007 | — | 2Q 17 | 2Q 17 | |||||||||

2100 Rideout Road Huntsville, Alabama (4) | Redstone Arsenal | Redstone Gateway | 19 | 58% | 5,123 | 4,578 | 3,100 | 2Q 16 | 2Q 17 | |||||||||

NOVA Office D Northern Virginia | NoVA Defense/IT | Other | 240 | 100% | 49,344 | 12,768 | — | 3Q 17 | 3Q 17 | |||||||||

540 National Business Parkway Annapolis Junction, Maryland | Ft. Meade/BW Corridor | National Bus. Park | 145 | 49% | 43,712 | 23,514 | — | 1Q 17 | 1Q 18 | |||||||||

Total Under Construction | 769 | 89% | $ | 149,700 | $ | 64,335 | $ | 3,100 | ||||||||||

Held for Lease to Government | ||||||||||||||||||

310 Sentinel Way Annapolis Junction, Maryland | Ft Meade/BW Corridor | National Bus. Park | 191 | 8% | 54,352 | 39,375 | 39,375 | (1) | (1) | |||||||||

NOVA Office B Northern Virginia | NoVA Defense/IT | Other | 161 | 0% | 41,500 | 31,304 | 31,304 | (1) | (1) | |||||||||

Total Held for Lease to Government | 352 | 4% | $ | 95,852 | $ | 70,679 | $ | 70,679 | ||||||||||

Total Construction Projects | 1,121 | 63% | $ | 245,552 | $ | 135,014 | $ | 73,779 | ||||||||||

(1) | Includes properties under, or contractually committed for, construction as of 9/30/16 and 310 Sentinel Way and NOVA Office B, two properties that were complete but held for future lease to the United States Government. |

(2) | Cost includes land, construction, leasing costs and allocated portion of structured parking and other shared infrastructure, if applicable. |

(3) | Anticipated operational date is the estimated date when leases have commenced on 100% of a property’s space or one year from the cessation of major construction activities. |

(4) | Although classified as under construction, 11,000 square feet were operational as of 9/30/16; NOI and cash NOI for this property was $22,000 for the three months ended 9/30/16. |

Property Segment | Park/Submarket | Total Rentable Square Feet | Percentage Leased as of 9/30/16 (2) | as of 9/30/16 (1) | Actual or Anticipated Shell Completion Date | Anticipated Operational Date (3) | |||||||||||||||||

Historical Basis, Net | Incremental Redevelopment Cost | Anticipated Total Cost | Cost to Date | Cost to Date Placed in Service | |||||||||||||||||||

Property and Location | |||||||||||||||||||||||

7134 Columbia Gateway Drive Columbia, Maryland (4) | Ft Meade/BW Corridor | Howard Co. Perimeter | 22 | 38% | $ | 1,703 | $ | 2,547 | $ | 4,250 | $ | 3,659 | $ | 2,213 | 1Q 16 | 1Q 17 | |||||||

1201 Winterson Rd (AS13) Linthicum, Maryland | Ft Meade/BW Corridor | Airport Square | 68 | 0% | 2,959 | 12,892 | 15,851 | 10,876 | 2,959 | 1Q 16 | 1Q 17 | ||||||||||||

Airport Landing (2) Linthicum, Maryland | Ft Meade/BW Corridor | Airport Square | |||||||||||||||||||||

Retail Buildings | 14 | 56% | 785 | 6,401 | 7,186 | 5,369 | 785 | 4Q 16 | 4Q 17 | ||||||||||||||

Pad Site | N/A | 100% | 259 | 183 | 442 | 442 | 259 | 4Q 16 | 4Q 16 | ||||||||||||||

Total Under Redevelopment | 104 | 19% | $ | 5,706 | $ | 22,023 | $ | 27,729 | $ | 20,346 | $ | 6,216 | |||||||||||

(1) | Cost includes construction, leasing costs and allocated portion of shared infrastructure. |

(2) | The redevelopment of Airport Landing involves the demolition of the existing office property to develop a retail center to serve the submarket. Upon completion, the project’s retail amenities will include: newly constructed retail property totaling 14,000 square feet; and a 1.2 acre retail pad site already under ground lease for 20 years to a national food service provider. The total percentage leased reported above for redevelopment projects was calculated by including the square footage of the building to be constructed on the pad site by the lessee. |

(3) | Anticipated operational date is the estimated date when leases have commenced on 100% of a property’s space or one year from the cessation of major construction activities. |

(4) | Although classified as under redevelopment, 4,000 square feet were operational as of 9/30/16; NOI and cash NOI for this property was $(3,000) for the three months ended 9/30/16. |

Total Property | ||||||||||||||||

% Leased as of 9/30/16 | Rentable Square Feet | Space Placed in Service % Leased as of 9/30/16 | ||||||||||||||

Property Segment | Park/Submarket | Square Feet Placed in Service in 2016 | ||||||||||||||

Property and Location | Prior Year | 1st Quarter | 2nd Quarter | 3rd Quarter | Total 2016 | |||||||||||

Patriot Point - DC15 Ashburn, Virginia | Data Center Shells | Ashburn | 100% | 149 | — | 149 | — | — | 149 | 100% | ||||||

Patriot Point - DC16 Ashburn, Virginia | Data Center Shells | Ashburn | 100% | 149 | — | — | 149 | — | 149 | 100% | ||||||

6708 Alexander Bell Drive Columbia, Maryland | Ft Meade/BW Corridor | Howard Co. Perimeter | 0% | 51 | — | 51 | — | — | 51 | 0% | ||||||

7134 Columbia Gateway Drive Columbia, Maryland | Ft Meade/BW Corridor | Howard Co. Perimeter | 36% | 22 | — | — | 4 | — | 4 | 100% | ||||||

Patriot Point - DC17 Ashburn, Virginia | Data Center Shells | Ashburn | 100% | 149 | — | — | — | 149 | 149 | 100% | ||||||

7880 Milestone Parkway Hanover, Maryland | Ft Meade/BW Corridor | Arundel Preserve | 73% | 120 | 88 | — | — | 32 | 32 | 73% | ||||||

2100 Rideout Road Huntsville, Alabama | Redstone Arsenal | Redstone Gateway | 58% | 19 | — | — | — | 11 | 11 | 100% | ||||||

Total Construction/Redevelopment Placed Into Service | 84% | 659 | 88 | 200 | 153 | 192 | 545 | 87% | ||||||||

Location | Acres | Estimated Developable Square Feet (in thousands) | Costs to Date (2) | ||||||

Land Owned/Controlled for Future Development | |||||||||