| Management | Investor Relations | |||||||

Stephen E. Budorick, President + CEO | Stephanie Krewson-Kelly, VP of IR | |||||||

Todd Hartman, EVP + COO | 443.285.5453 // stephanie.kelly@copt.com | |||||||

Anthony Mifsud, EVP + CFO | ||||||||

| Michelle Layne, Manager of IR | ||||||||

443.285.5452 // michelle.layne@copt.com | ||||||||

| Firm | Senior Analyst | Phone | ||||||||||||||||||

| Bank of America Securities | Jamie Feldman | 646-855-5808 | james.feldman@bofa.com | |||||||||||||||||

| BTIG | Tom Catherwood | 212-738-6410 | tcatherwood@btig.com | |||||||||||||||||

| Capital One Securities | Chris Lucas | 571-633-8151 | christopher.lucas@capitalone.com | |||||||||||||||||

| Citigroup Global Markets | Manny Korchman | 212-816-1382 | emmanuel.korchman@citi.com | |||||||||||||||||

| Evercore ISI | Steve Sakwa | 212-446-9462 | steve.sakwa@evercoreisi.com | |||||||||||||||||

| Green Street | Daniel Ismail | 949-640-8780 | dismail@greenstreet.com | |||||||||||||||||

| Jefferies & Co. | Peter Abramowitz | 212-336-7241 | pabramowitz@jefferies.com | |||||||||||||||||

| JP Morgan | Tony Paolone | 212-622-6682 | anthony.paolone@jpmorgan.com | |||||||||||||||||

| KeyBanc Capital Markets | Craig Mailman | 917-368-2316 | cmailman@key.com | |||||||||||||||||

| Raymond James | Bill Crow | 727-567-2594 | bill.crow@raymondjames.com | |||||||||||||||||

| Robert W. Baird & Co., Inc. | Dave Rodgers | 216-737-7341 | drodgers@rwbaird.com | |||||||||||||||||

| SMBC Nikko Securities America, Inc. | Rich Anderson | 646-521-2351 | randerson@smbcnikko-si.com | |||||||||||||||||

| Truist Securities | Michael Lewis | 212-319-5659 | michael.r.lewis@truist.com | |||||||||||||||||

| Wells Fargo Securities | Blaine Heck | 443-263-6529 | blaine.heck@wellsfargo.com | |||||||||||||||||

| Page | Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||||||||||

| SUMMARY OF RESULTS | Refer. | 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | ||||||||||||||||||||||||||||||||||||||||||

| Net income (loss) | 6 | $ | 14,965 | $ | 28,794 | $ | 43,898 | $ | (6,079) | $ | 83,549 | $ | 81,578 | $ | 102,878 | |||||||||||||||||||||||||||||||||||

| NOI from real estate operations | 13 | $ | 90,523 | $ | 90,460 | $ | 90,780 | $ | 89,107 | $ | 89,304 | $ | 360,870 | $ | 341,836 | |||||||||||||||||||||||||||||||||||

| Same Properties NOI | 16 | $ | 73,691 | $ | 76,728 | $ | 76,819 | $ | 74,369 | $ | 75,633 | $ | 301,607 | $ | 299,830 | |||||||||||||||||||||||||||||||||||

| Same Properties cash NOI | 17 | $ | 76,866 | $ | 77,219 | $ | 77,429 | $ | 72,664 | $ | 76,515 | $ | 304,178 | $ | 300,539 | |||||||||||||||||||||||||||||||||||

| Adjusted EBITDA | 10 | $ | 84,681 | $ | 83,991 | $ | 85,186 | $ | 83,338 | $ | 82,298 | $ | 337,196 | $ | 318,931 | |||||||||||||||||||||||||||||||||||

| Diluted AFFO avail. to common share and unit holders | 9 | $ | 32,823 | $ | 53,635 | $ | 54,781 | $ | 52,387 | $ | 56,792 | $ | 193,256 | $ | 195,317 | |||||||||||||||||||||||||||||||||||

| Dividend per common share | N/A | $ | 0.275 | $ | 0.275 | $ | 0.275 | $ | 0.275 | $ | 0.275 | $ | 1.10 | $ | 1.10 | |||||||||||||||||||||||||||||||||||

| Per share - diluted: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| EPS | 8 | $ | 0.12 | $ | 0.24 | $ | 0.38 | $ | (0.06) | $ | 0.73 | $ | 0.68 | $ | 0.87 | |||||||||||||||||||||||||||||||||||

| FFO - Nareit | 8 | $ | 0.21 | $ | 0.56 | $ | 0.35 | $ | 0.27 | $ | 0.53 | $ | 1.40 | $ | 1.50 | |||||||||||||||||||||||||||||||||||

| FFO - as adjusted for comparability | 8 | $ | 0.58 | $ | 0.57 | $ | 0.58 | $ | 0.56 | $ | 0.56 | $ | 2.29 | $ | 2.12 | |||||||||||||||||||||||||||||||||||

| Numerators for diluted per share amounts: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Diluted EPS | 6 | $ | 13,546 | $ | 26,933 | $ | 42,256 | $ | (6,839) | $ | 81,501 | $ | 75,996 | $ | 96,970 | |||||||||||||||||||||||||||||||||||

| Diluted FFO available to common share and unit holders | 7 | $ | 24,344 | $ | 63,898 | $ | 40,212 | $ | 30,997 | $ | 60,137 | $ | 159,563 | $ | 169,728 | |||||||||||||||||||||||||||||||||||

| Diluted FFO available to common share and unit holders, as adjusted for comparability | 7 | $ | 65,458 | $ | 65,179 | $ | 65,605 | $ | 64,454 | $ | 64,188 | $ | 260,326 | $ | 241,356 | |||||||||||||||||||||||||||||||||||

| Payout ratios: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Diluted FFO | N/A | 128.0% | 48.8% | 77.5% | 100.5% | 51.8% | 78.1% | 73.3% | ||||||||||||||||||||||||||||||||||||||||||

| Diluted FFO - as adjusted for comparability | N/A | 47.6% | 47.8% | 47.5% | 48.3% | 48.6% | 47.9% | 51.7% | ||||||||||||||||||||||||||||||||||||||||||

| Diluted AFFO | N/A | 95.0% | 58.1% | 56.9% | 59.5% | 54.9% | 64.5% | 63.8% | ||||||||||||||||||||||||||||||||||||||||||

| CAPITALIZATION | ||||||||||||||||||||||||||||||||||||||||||||||||||

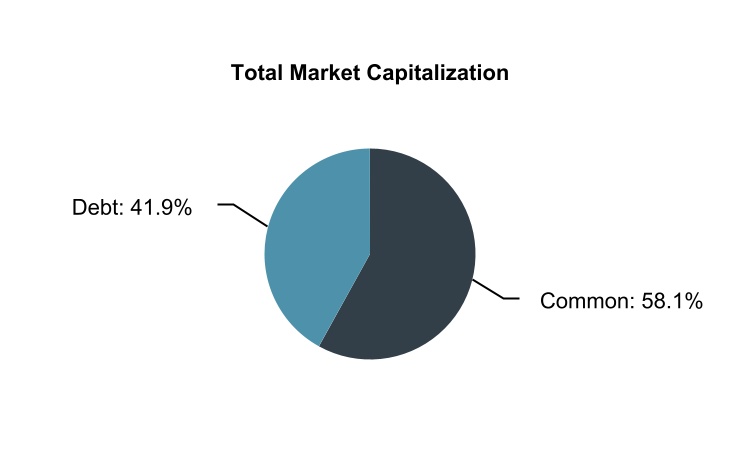

| Total Market Capitalization | 28 | $ | 5,479,985 | $ | 5,251,729 | $ | 5,315,385 | $ | 5,226,694 | $ | 5,062,432 | |||||||||||||||||||||||||||||||||||||||

| Total Equity Market Capitalization | 28 | $ | 3,181,699 | $ | 3,069,056 | $ | 3,184,310 | $ | 2,995,090 | $ | 2,960,967 | |||||||||||||||||||||||||||||||||||||||

| Gross debt | 29 | $ | 2,324,536 | $ | 2,208,923 | $ | 2,157,325 | $ | 2,257,854 | $ | 2,127,715 | |||||||||||||||||||||||||||||||||||||||

| Net debt to adjusted book | 31 | 40.5% | 39.4% | 39.4% | 40.8% | 39.1% | N/A | N/A | ||||||||||||||||||||||||||||||||||||||||||

| Adjusted EBITDA fixed charge coverage ratio | 31 | 4.9x | 4.8x | 4.9x | 4.3x | 4.1x | 4.7x | 3.9x | ||||||||||||||||||||||||||||||||||||||||||

| Net debt to in-place adj. EBITDA ratio | 31 | 6.7x | 6.3x | 6.3x | 6.6x | 6.2x | N/A | N/A | ||||||||||||||||||||||||||||||||||||||||||

| Pro forma net debt to in-place adjusted EBITDA ratio (1) | 31 | 6.3x | N/A | N/A | N/A | N/A | N/A | N/A | ||||||||||||||||||||||||||||||||||||||||||

| Net debt adjusted for fully-leased development to in-place adj. EBITDA ratio | 31 | 6.2x | 5.9x | 5.8x | 6.3x | 5.9x | N/A | N/A | ||||||||||||||||||||||||||||||||||||||||||

| Pro forma net debt adj. for fully-leased development to in-place adj. EBITDA ratio (1) | 31 | 5.8x | N/A | N/A | N/A | N/A | N/A | N/A | ||||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | |||||||||||||||||||||||||

| Operating Office and Data Center Shell Properties | |||||||||||||||||||||||||||||

| # of Properties | |||||||||||||||||||||||||||||

| Total Portfolio | 186 | 186 | 184 | 182 | 181 | ||||||||||||||||||||||||

| Consolidated Portfolio | 167 | 167 | 165 | 165 | 164 | ||||||||||||||||||||||||

| Core Portfolio | 184 | 184 | 182 | 180 | 179 | ||||||||||||||||||||||||

| Same Properties | 159 | 159 | 159 | 159 | 159 | ||||||||||||||||||||||||

| % Occupied | |||||||||||||||||||||||||||||

| Total Portfolio | 92.4 | % | 93.3 | % | 93.2 | % | 93.8 | % | 94.1 | % | |||||||||||||||||||

| Consolidated Portfolio | 91.1 | % | 92.2 | % | 92.0 | % | 92.9 | % | 93.2 | % | |||||||||||||||||||

| Core Portfolio | 92.6 | % | 93.5 | % | 93.4 | % | 94.0 | % | 94.3 | % | |||||||||||||||||||

| Same Properties | 91.3 | % | 92.2 | % | 92.2 | % | 92.6 | % | 92.9 | % | |||||||||||||||||||

| % Leased | |||||||||||||||||||||||||||||

| Total Portfolio | 94.2 | % | 94.6 | % | 94.1 | % | 94.7 | % | 94.8 | % | |||||||||||||||||||

| Consolidated Portfolio | 93.2 | % | 93.7 | % | 93.0 | % | 93.9 | % | 94.0 | % | |||||||||||||||||||

| Core Portfolio | 94.4 | % | 94.8 | % | 94.3 | % | 94.9 | % | 95.0 | % | |||||||||||||||||||

| Same Properties | 93.4 | % | 93.7 | % | 93.2 | % | 93.6 | % | 93.8 | % | |||||||||||||||||||

| Square Feet (in thousands) | |||||||||||||||||||||||||||||

| Total Portfolio | 21,710 | 21,660 | 21,198 | 21,006 | 20,959 | ||||||||||||||||||||||||

| Consolidated Portfolio | 18,529 | 18,479 | 18,016 | 18,257 | 18,209 | ||||||||||||||||||||||||

| Core Portfolio | 21,553 | 21,503 | 21,041 | 20,849 | 20,802 | ||||||||||||||||||||||||

| Same Properties | 17,357 | 17,357 | 17,357 | 17,357 | 17,357 | ||||||||||||||||||||||||

| Wholesale Data Center | |||||||||||||||||||||||||||||

| Megawatts Operational | 19.25 | 19.25 | 19.25 | 19.25 | 19.25 | ||||||||||||||||||||||||

| % Leased | 86.7 | % | 86.7 | % | 86.7 | % | 86.7 | % | 86.7 | % | |||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | |||||||||||||||||||||||||

| Assets | |||||||||||||||||||||||||||||

| Properties, net: | |||||||||||||||||||||||||||||

| Operating properties, net | $ | 3,090,510 | $ | 3,034,365 | $ | 2,904,129 | $ | 2,908,986 | $ | 2,915,016 | |||||||||||||||||||

| Development and redevelopment in progress, including land (1) | 196,701 | 151,396 | 201,421 | 187,290 | 172,614 | ||||||||||||||||||||||||

| Land held (1) | 245,733 | 227,887 | 230,114 | 285,266 | 274,655 | ||||||||||||||||||||||||

| Total properties, net | 3,532,944 | 3,413,648 | 3,335,664 | 3,381,542 | 3,362,285 | ||||||||||||||||||||||||

| Property - operating right-of-use assets | 38,361 | 38,854 | 39,333 | 39,810 | 40,570 | ||||||||||||||||||||||||

| Property - finance right-of-use assets | 2,238 | 40,077 | 40,082 | 40,091 | 40,425 | ||||||||||||||||||||||||

| Assets held for sale, net (2) | 192,699 | 197,285 | 196,210 | 199,028 | 201,820 | ||||||||||||||||||||||||

| Cash and cash equivalents | 13,262 | 14,570 | 17,182 | 36,139 | 18,369 | ||||||||||||||||||||||||

| Investment in unconsolidated real estate joint ventures | 39,889 | 40,304 | 40,586 | 28,934 | 29,303 | ||||||||||||||||||||||||

| Accounts receivable, net | 40,752 | 33,110 | 39,951 | 44,916 | 41,637 | ||||||||||||||||||||||||

| Deferred rent receivable | 108,926 | 102,479 | 99,006 | 97,222 | 91,851 | ||||||||||||||||||||||||

| Intangible assets on property acquisitions, net | 14,567 | 15,711 | 16,877 | 18,048 | 19,249 | ||||||||||||||||||||||||

| Deferred leasing costs, net | 65,850 | 61,939 | 61,911 | 56,107 | 58,177 | ||||||||||||||||||||||||

| Investing receivables, net | 82,226 | 75,947 | 73,073 | 71,831 | 68,754 | ||||||||||||||||||||||||

| Prepaid expenses and other assets, net | 130,738 | 117,214 | 92,157 | 99,280 | 104,583 | ||||||||||||||||||||||||

| Total assets | $ | 4,262,452 | $ | 4,151,138 | $ | 4,052,032 | $ | 4,112,948 | $ | 4,077,023 | |||||||||||||||||||

| Liabilities and equity | |||||||||||||||||||||||||||||

| Liabilities: | |||||||||||||||||||||||||||||

| Debt | $ | 2,272,304 | $ | 2,159,732 | $ | 2,109,640 | $ | 2,207,903 | $ | 2,086,918 | |||||||||||||||||||

| Accounts payable and accrued expenses | 186,202 | 176,636 | 127,027 | 96,465 | 142,717 | ||||||||||||||||||||||||

| Rents received in advance and security deposits | 32,262 | 32,092 | 30,893 | 30,922 | 33,425 | ||||||||||||||||||||||||

| Dividends and distributions payable | 31,299 | 31,306 | 31,302 | 31,305 | 31,231 | ||||||||||||||||||||||||

| Deferred revenue associated with operating leases | 9,341 | 8,704 | 9,564 | 10,221 | 10,832 | ||||||||||||||||||||||||

| Property - operating lease liabilities | 29,342 | 29,630 | 29,909 | 30,176 | 30,746 | ||||||||||||||||||||||||

| Interest rate derivatives | 3,644 | 5,562 | 6,646 | 7,640 | 9,522 | ||||||||||||||||||||||||

| Other liabilities | 14,085 | 10,691 | 9,699 | 15,599 | 12,490 | ||||||||||||||||||||||||

| Total liabilities | 2,578,479 | 2,454,353 | 2,354,680 | 2,430,231 | 2,357,881 | ||||||||||||||||||||||||

| Redeemable noncontrolling interests | 26,898 | 26,006 | 26,040 | 25,925 | 25,430 | ||||||||||||||||||||||||

| Equity: | |||||||||||||||||||||||||||||

| COPT’s shareholders’ equity: | |||||||||||||||||||||||||||||

| Common shares | 1,123 | 1,123 | 1,123 | 1,123 | 1,122 | ||||||||||||||||||||||||

| Additional paid-in capital | 2,481,539 | 2,480,412 | 2,478,416 | 2,476,807 | 2,478,906 | ||||||||||||||||||||||||

| Cumulative distributions in excess of net income | (856,863) | (839,676) | (835,894) | (847,407) | (809,836) | ||||||||||||||||||||||||

| Accumulated other comprehensive loss | (3,059) | (5,347) | (6,415) | (7,391) | (9,157) | ||||||||||||||||||||||||

| Total COPT’s shareholders’ equity | 1,622,740 | 1,636,512 | 1,637,230 | 1,623,132 | 1,661,035 | ||||||||||||||||||||||||

| Noncontrolling interests in subsidiaries: | |||||||||||||||||||||||||||||

| Common units in the Operating Partnership | 21,363 | 21,568 | 21,604 | 21,345 | 20,465 | ||||||||||||||||||||||||

| Other consolidated entities | 12,972 | 12,699 | 12,478 | 12,315 | 12,212 | ||||||||||||||||||||||||

| Total noncontrolling interests in subsidiaries | 34,335 | 34,267 | 34,082 | 33,660 | 32,677 | ||||||||||||||||||||||||

| Total equity | 1,657,075 | 1,670,779 | 1,671,312 | 1,656,792 | 1,693,712 | ||||||||||||||||||||||||

| Total liabilities, redeemable noncontrolling interests and equity | $ | 4,262,452 | $ | 4,151,138 | $ | 4,052,032 | $ | 4,112,948 | $ | 4,077,023 | |||||||||||||||||||

| Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||

| Revenues | |||||||||||||||||||||||||||||||||||||||||

| Lease revenue | $ | 141,892 | $ | 138,032 | $ | 136,454 | $ | 137,290 | $ | 131,672 | $ | 553,668 | $ | 509,114 | |||||||||||||||||||||||||||

| Other property revenue | 756 | 841 | 765 | 540 | 535 | 2,902 | 2,600 | ||||||||||||||||||||||||||||||||||

| Construction contract and other service revenues | 43,284 | 28,046 | 19,988 | 16,558 | 24,400 | 107,876 | 70,640 | ||||||||||||||||||||||||||||||||||

| Total revenues | 185,932 | 166,919 | 157,207 | 154,388 | 156,607 | 664,446 | 582,354 | ||||||||||||||||||||||||||||||||||

| Operating expenses | |||||||||||||||||||||||||||||||||||||||||

| Property operating expenses | 56,459 | 52,728 | 50,914 | 53,276 | 48,870 | 213,377 | 190,796 | ||||||||||||||||||||||||||||||||||

| Depreciation and amortization associated with real estate operations | 34,504 | 33,807 | 34,732 | 34,500 | 33,814 | 137,543 | 126,503 | ||||||||||||||||||||||||||||||||||

| Construction contract and other service expenses | 42,089 | 27,089 | 19,082 | 15,793 | 23,563 | 104,053 | 67,615 | ||||||||||||||||||||||||||||||||||

| Impairment losses | — | — | — | — | — | — | 1,530 | ||||||||||||||||||||||||||||||||||

| General and administrative expenses | 6,589 | 7,269 | 7,293 | 6,062 | 7,897 | 27,213 | 25,269 | ||||||||||||||||||||||||||||||||||

| Leasing expenses | 2,568 | 2,073 | 1,929 | 2,344 | 1,993 | 8,914 | 7,732 | ||||||||||||||||||||||||||||||||||

| Business development expenses and land carry costs | 1,088 | 1,093 | 1,372 | 1,094 | 999 | 4,647 | 4,473 | ||||||||||||||||||||||||||||||||||

| Total operating expenses | 143,297 | 124,059 | 115,322 | 113,069 | 117,136 | 495,747 | 423,918 | ||||||||||||||||||||||||||||||||||

| Interest expense | (16,217) | (15,720) | (15,942) | (17,519) | (17,148) | (65,398) | (67,937) | ||||||||||||||||||||||||||||||||||

| Interest and other income | 1,968 | 1,818 | 2,228 | 1,865 | 3,341 | 7,879 | 8,574 | ||||||||||||||||||||||||||||||||||

| Credit loss recoveries (expense) | 88 | 326 | (193) | 907 | 772 | 1,128 | 933 | ||||||||||||||||||||||||||||||||||

| Gain on sales of real estate | 25,879 | (32) | 40,233 | (490) | 30,204 | 65,590 | 30,209 | ||||||||||||||||||||||||||||||||||

| Gain on sale of investment in unconsolidated real estate joint venture | — | — | — | — | 29,416 | — | 29,416 | ||||||||||||||||||||||||||||||||||

| Loss on early extinguishment of debt | (41,073) | (1,159) | (25,228) | (33,166) | (4,069) | (100,626) | (7,306) | ||||||||||||||||||||||||||||||||||

| Loss on interest rate derivatives | — | — | — | — | — | — | (53,196) | ||||||||||||||||||||||||||||||||||

| Income (loss) from continuing operations before equity in income of unconsolidated entities and income taxes | 13,280 | 28,093 | 42,983 | (7,084) | 81,987 | 77,272 | 99,129 | ||||||||||||||||||||||||||||||||||

| Equity in income of unconsolidated entities | 314 | 297 | 260 | 222 | 453 | 1,093 | 1,825 | ||||||||||||||||||||||||||||||||||

| Income tax expense | (42) | (47) | (24) | (32) | (258) | (145) | (353) | ||||||||||||||||||||||||||||||||||

| Income from continuing operations | 13,552 | 28,343 | 43,219 | (6,894) | 82,182 | 78,220 | 100,601 | ||||||||||||||||||||||||||||||||||

| Discontinued operations | 1,413 | 451 | 679 | 815 | 1,367 | 3,358 | 2,277 | ||||||||||||||||||||||||||||||||||

| Net income (loss) | 14,965 | 28,794 | 43,898 | (6,079) | 83,549 | 81,578 | 102,878 | ||||||||||||||||||||||||||||||||||

| Net (income) loss attributable to noncontrolling interests: | |||||||||||||||||||||||||||||||||||||||||

| Common units in the Operating Partnership | (181) | (357) | (559) | 85 | (995) | (1,012) | (1,180) | ||||||||||||||||||||||||||||||||||

| Preferred units in the Operating Partnership | — | — | — | — | (69) | — | (300) | ||||||||||||||||||||||||||||||||||

| Other consolidated entities | (1,076) | (1,336) | (938) | (675) | (817) | (4,025) | (4,024) | ||||||||||||||||||||||||||||||||||

| Net income (loss) attributable to COPT common shareholders | $ | 13,708 | $ | 27,101 | $ | 42,401 | $ | (6,669) | $ | 81,668 | $ | 76,541 | $ | 97,374 | |||||||||||||||||||||||||||

| Amount allocable to share-based compensation awards | (116) | (79) | (125) | (170) | (280) | (417) | (404) | ||||||||||||||||||||||||||||||||||

| Redeemable noncontrolling interests | (46) | (89) | (20) | — | 44 | (128) | — | ||||||||||||||||||||||||||||||||||

| Distributions on dilutive convertible preferred units | — | — | — | — | 69 | — | — | ||||||||||||||||||||||||||||||||||

| Numerator for diluted EPS | $ | 13,546 | $ | 26,933 | $ | 42,256 | $ | (6,839) | $ | 81,501 | $ | 75,996 | $ | 96,970 | |||||||||||||||||||||||||||

| Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||

| Net income (loss) | $ | 14,965 | $ | 28,794 | $ | 43,898 | $ | (6,079) | $ | 83,549 | $ | 81,578 | $ | 102,878 | |||||||||||||||||||||||||||

| Real estate-related depreciation and amortization | 36,346 | 36,611 | 37,555 | 37,321 | 36,653 | 147,833 | 138,193 | ||||||||||||||||||||||||||||||||||

| Impairment losses on real estate | — | — | — | — | — | — | 1,530 | ||||||||||||||||||||||||||||||||||

| Gain on sales of real estate | (25,879) | 32 | (40,233) | 490 | (30,204) | (65,590) | (30,209) | ||||||||||||||||||||||||||||||||||

| Depreciation and amortization on unconsolidated real estate JVs (1) | 526 | 525 | 476 | 454 | 874 | 1,981 | 3,329 | ||||||||||||||||||||||||||||||||||

| Gain on sale of investment in unconsolidated real estate JV | — | — | — | — | (29,416) | — | (29,416) | ||||||||||||||||||||||||||||||||||

| FFO - per Nareit (2)(3) | 25,958 | 65,962 | 41,696 | 32,186 | 61,456 | 165,802 | 186,305 | ||||||||||||||||||||||||||||||||||

| Noncontrolling interests - preferred units in the Operating Partnership | — | — | — | — | (69) | — | (300) | ||||||||||||||||||||||||||||||||||

| FFO allocable to other noncontrolling interests (4) | (1,458) | (1,696) | (1,302) | (1,027) | (1,091) | (5,483) | (15,705) | ||||||||||||||||||||||||||||||||||

| Basic FFO allocable to share-based compensation awards | (149) | (313) | (193) | (162) | (272) | (777) | (719) | ||||||||||||||||||||||||||||||||||

| Basic FFO available to common share and common unit holders (3) | 24,351 | 63,953 | 40,201 | 30,997 | 60,024 | 159,542 | 169,581 | ||||||||||||||||||||||||||||||||||

| Dilutive preferred units in the Operating Partnership | — | — | — | — | 69 | — | — | ||||||||||||||||||||||||||||||||||

| Redeemable noncontrolling interests | (13) | (68) | 11 | — | 44 | (11) | 147 | ||||||||||||||||||||||||||||||||||

| Diluted FFO adjustments allocable to share-based compensation awards | 6 | 13 | — | — | — | 32 | — | ||||||||||||||||||||||||||||||||||

| Diluted FFO available to common share and common unit holders - per Nareit (3) | 24,344 | 63,898 | 40,212 | 30,997 | 60,137 | 159,563 | 169,728 | ||||||||||||||||||||||||||||||||||

| Loss on early extinguishment of debt | 41,073 | 1,159 | 25,228 | 33,166 | 4,069 | 100,626 | 7,306 | ||||||||||||||||||||||||||||||||||

| Loss on interest rate derivatives | — | — | — | — | — | — | 53,196 | ||||||||||||||||||||||||||||||||||

| Loss on interest rate derivatives included in interest expense | 221 | — | — | — | — | 221 | — | ||||||||||||||||||||||||||||||||||

| Demolition costs on redevelopment and nonrecurring improvements | (8) | 129 | 302 | — | — | 423 | 63 | ||||||||||||||||||||||||||||||||||

| Dilutive preferred units in the Operating Partnership | — | — | — | — | — | — | 300 | ||||||||||||||||||||||||||||||||||

| FFO allocation to other noncontrolling interests resulting from capital event (4) | — | — | — | — | — | — | 11,090 | ||||||||||||||||||||||||||||||||||

| Diluted FFO comparability adjustments for redeemable noncontrolling interests | — | — | — | 458 | — | — | — | ||||||||||||||||||||||||||||||||||

| Diluted FFO comparability adjustments allocable to share-based compensation awards | (172) | (7) | (137) | (167) | (18) | (507) | (327) | ||||||||||||||||||||||||||||||||||

| Diluted FFO available to common share and common unit holders, as adjusted for comparability (3) | $ | 65,458 | $ | 65,179 | $ | 65,605 | $ | 64,454 | $ | 64,188 | $ | 260,326 | $ | 241,356 | |||||||||||||||||||||||||||

| Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||

| EPS Denominator: | |||||||||||||||||||||||||||||||||||||||||

| Weighted average common shares - basic | 111,990 | 111,985 | 111,974 | 111,888 | 111,817 | 111,960 | 111,788 | ||||||||||||||||||||||||||||||||||

| Dilutive effect of share-based compensation awards | 386 | 375 | 297 | — | 320 | 330 | 288 | ||||||||||||||||||||||||||||||||||

| Dilutive effect of redeemable noncontrolling interests | 124 | 138 | 133 | — | 117 | 128 | — | ||||||||||||||||||||||||||||||||||

| Dilutive convertible preferred units | — | — | — | — | 155 | — | — | ||||||||||||||||||||||||||||||||||

| Weighted average common shares - diluted | 112,500 | 112,498 | 112,404 | 111,888 | 112,409 | 112,418 | 112,076 | ||||||||||||||||||||||||||||||||||

| Diluted EPS | $ | 0.12 | $ | 0.24 | $ | 0.38 | $ | (0.06) | $ | 0.73 | $ | 0.68 | $ | 0.87 | |||||||||||||||||||||||||||

| Weighted Average Shares for period ended: | |||||||||||||||||||||||||||||||||||||||||

| Common shares | 111,990 | 111,985 | 111,974 | 111,888 | 111,817 | 111,960 | 111,788 | ||||||||||||||||||||||||||||||||||

| Dilutive effect of share-based compensation awards | 386 | 375 | 297 | 261 | 320 | 330 | 288 | ||||||||||||||||||||||||||||||||||

| Common units | 1,259 | 1,262 | 1,262 | 1,246 | 1,239 | 1,257 | 1,236 | ||||||||||||||||||||||||||||||||||

| Redeemable noncontrolling interests | 124 | 138 | 133 | — | 117 | 128 | 123 | ||||||||||||||||||||||||||||||||||

| Dilutive convertible preferred units | — | — | — | — | 155 | — | — | ||||||||||||||||||||||||||||||||||

| Denominator for diluted FFO per share | 113,759 | 113,760 | 113,666 | 113,395 | 113,648 | 113,675 | 113,435 | ||||||||||||||||||||||||||||||||||

| Redeemable noncontrolling interests | — | — | — | 940 | — | — | — | ||||||||||||||||||||||||||||||||||

| Dilutive convertible preferred units | — | — | — | — | — | — | 171 | ||||||||||||||||||||||||||||||||||

| Denominator for diluted FFO per share, as adjusted for comparability | 113,759 | 113,760 | 113,666 | 114,335 | 113,648 | 113,675 | 113,606 | ||||||||||||||||||||||||||||||||||

| Weighted average common units | (1,259) | (1,262) | (1,262) | (1,246) | (1,239) | (1,257) | (1,236) | ||||||||||||||||||||||||||||||||||

| Redeemable noncontrolling interests | — | — | — | (940) | — | — | (123) | ||||||||||||||||||||||||||||||||||

| Anti-dilutive EPS effect of share-based compensation awards | — | — | — | (261) | — | — | — | ||||||||||||||||||||||||||||||||||

| Dilutive convertible preferred units | — | — | — | — | — | — | (171) | ||||||||||||||||||||||||||||||||||

| Denominator for diluted EPS | 112,500 | 112,498 | 112,404 | 111,888 | 112,409 | 112,418 | 112,076 | ||||||||||||||||||||||||||||||||||

| Diluted FFO per share - Nareit | $ | 0.21 | $ | 0.56 | $ | 0.35 | $ | 0.27 | $ | 0.53 | $ | 1.40 | $ | 1.50 | |||||||||||||||||||||||||||

| Diluted FFO per share - as adjusted for comparability | $ | 0.58 | $ | 0.57 | $ | 0.58 | $ | 0.56 | $ | 0.56 | $ | 2.29 | $ | 2.12 | |||||||||||||||||||||||||||

| Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||

| Diluted FFO available to common share and common unit holders, as adjusted for comparability | $ | 65,458 | $ | 65,179 | $ | 65,605 | $ | 64,454 | $ | 64,188 | $ | 260,326 | $ | 241,356 | |||||||||||||||||||||||||||

| Straight line rent adjustments and lease incentive amortization | (3,835) | (1,806) | (1,288) | (3,357) | 3,438 | (10,286) | 4,100 | ||||||||||||||||||||||||||||||||||

| Amortization of intangibles and other assets included in NOI | 40 | 41 | 41 | 40 | 24 | 162 | (162) | ||||||||||||||||||||||||||||||||||

| Share-based compensation, net of amounts capitalized | 2,018 | 2,048 | 2,009 | 1,904 | 1,751 | 7,979 | 6,505 | ||||||||||||||||||||||||||||||||||

| Amortization of deferred financing costs | 640 | 736 | 811 | 793 | 664 | 2,980 | 2,539 | ||||||||||||||||||||||||||||||||||

| Amortization of net debt discounts, net of amounts capitalized | 615 | 567 | 520 | 542 | 504 | 2,244 | 1,733 | ||||||||||||||||||||||||||||||||||

| Replacement capital expenditures (1) | (32,317) | (13,331) | (13,095) | (12,230) | (13,973) | (70,973) | (60,944) | ||||||||||||||||||||||||||||||||||

| Other | 204 | 201 | 178 | 241 | 196 | 824 | 190 | ||||||||||||||||||||||||||||||||||

| Diluted AFFO available to common share and common unit holders (“diluted AFFO”) | $ | 32,823 | $ | 53,635 | $ | 54,781 | $ | 52,387 | $ | 56,792 | $ | 193,256 | $ | 195,317 | |||||||||||||||||||||||||||

| Replacement capital expenditures (1) | |||||||||||||||||||||||||||||||||||||||||

| Tenant improvements and incentives | $ | 19,724 | $ | 8,654 | $ | 8,303 | $ | 7,139 | $ | 9,165 | $ | 43,820 | $ | 36,342 | |||||||||||||||||||||||||||

| Building improvements | 17,778 | 7,793 | 6,771 | 3,628 | 7,523 | 35,970 | 34,060 | ||||||||||||||||||||||||||||||||||

| Leasing costs | 5,863 | 2,939 | 2,805 | 1,129 | 1,514 | 12,736 | 8,432 | ||||||||||||||||||||||||||||||||||

| Net (exclusions from) additions to tenant improvements and incentives | (5,093) | (1,523) | (988) | 2,900 | (370) | (4,704) | 1,042 | ||||||||||||||||||||||||||||||||||

| Excluded building improvements and leasing costs | (5,955) | (4,532) | (3,796) | (2,566) | (3,859) | (16,849) | (18,932) | ||||||||||||||||||||||||||||||||||

| Replacement capital expenditures | $ | 32,317 | $ | 13,331 | $ | 13,095 | $ | 12,230 | $ | 13,973 | $ | 70,973 | $ | 60,944 | |||||||||||||||||||||||||||

| Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||

| Net income (loss) | $ | 14,965 | $ | 28,794 | $ | 43,898 | $ | (6,079) | $ | 83,549 | $ | 81,578 | $ | 102,878 | |||||||||||||||||||||||||||

| Interest expense | 16,217 | 15,720 | 15,942 | 17,519 | 17,148 | 65,398 | 67,937 | ||||||||||||||||||||||||||||||||||

| Income tax expense | 42 | 47 | 24 | 32 | 258 | 145 | 353 | ||||||||||||||||||||||||||||||||||

| Real estate-related depreciation and amortization | 36,346 | 36,611 | 37,555 | 37,321 | 36,653 | 147,833 | 138,193 | ||||||||||||||||||||||||||||||||||

| Other depreciation and amortization | 622 | 589 | 1,045 | 555 | 513 | 2,811 | 1,837 | ||||||||||||||||||||||||||||||||||

| Impairment losses on real estate | — | — | — | — | — | — | 1,530 | ||||||||||||||||||||||||||||||||||

| Gain on sales of real estate | (25,879) | 32 | (40,233) | 490 | (30,204) | (65,590) | (30,209) | ||||||||||||||||||||||||||||||||||

| Gain on sale of investment in unconsolidated real estate JV | — | — | — | — | (29,416) | — | (29,416) | ||||||||||||||||||||||||||||||||||

| Adjustments from unconsolidated real estate JVs | 763 | 763 | 711 | 693 | 1,306 | 2,930 | 5,120 | ||||||||||||||||||||||||||||||||||

| EBITDAre | 43,076 | 82,556 | 58,942 | 50,531 | 79,807 | 235,105 | 258,223 | ||||||||||||||||||||||||||||||||||

| Loss on early extinguishment of debt | 41,073 | 1,159 | 25,228 | 33,166 | 4,069 | 100,626 | 7,306 | ||||||||||||||||||||||||||||||||||

| Loss on interest rate derivatives | — | — | — | — | — | — | 53,196 | ||||||||||||||||||||||||||||||||||

| Net gain on other investments | — | — | (63) | — | (1,218) | (63) | (966) | ||||||||||||||||||||||||||||||||||

| Credit loss (recoveries) expense | (88) | (326) | 193 | (907) | (772) | (1,128) | (933) | ||||||||||||||||||||||||||||||||||

| Business development expenses | 628 | 473 | 584 | 548 | 412 | 2,233 | 2,042 | ||||||||||||||||||||||||||||||||||

| Demolition costs on redevelopment and nonrecurring improvements | (8) | 129 | 302 | — | — | 423 | 63 | ||||||||||||||||||||||||||||||||||

| Adjusted EBITDA | 84,681 | 83,991 | 85,186 | 83,338 | 82,298 | $ | 337,196 | $ | 318,931 | ||||||||||||||||||||||||||||||||

| Pro forma NOI adjustment for property changes within period | — | 3,240 | (379) | 166 | 1,459 | ||||||||||||||||||||||||||||||||||||

| Change in collectability of deferred rental revenue | — | — | — | 124 | 678 | ||||||||||||||||||||||||||||||||||||

| Other | 1,578 | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| In-place adjusted EBITDA | 86,259 | 87,231 | 84,807 | 83,628 | 84,435 | ||||||||||||||||||||||||||||||||||||

| Pro forma NOI adjustment for sale of Wholesale Data Center | (3,074) | N/A | N/A | N/A | N/A | ||||||||||||||||||||||||||||||||||||

| Pro forma in-place adjusted EBITDA | $ | 83,185 | $ | 87,231 | $ | 84,807 | $ | 83,628 | $ | 84,435 | |||||||||||||||||||||||||||||||

| # of Properties | Operational Square Feet | % Occupied | % Leased | |||||||||||||||||||||||

| Core Portfolio: | ||||||||||||||||||||||||||

| Defense/IT Locations: | ||||||||||||||||||||||||||

| Fort Meade/Baltimore Washington (“BW”) Corridor: | ||||||||||||||||||||||||||

| National Business Park | 32 | 3,926 | 92.8% | 95.1% | ||||||||||||||||||||||

| Howard County | 35 | 2,851 | 86.2% | 92.4% | ||||||||||||||||||||||

| Other | 23 | 1,725 | 89.7% | 91.2% | ||||||||||||||||||||||

| Total Fort Meade/BW Corridor | 90 | 8,502 | 90.0% | 93.4% | ||||||||||||||||||||||

| Northern Virginia (“NoVA”) Defense/IT | 14 | 2,336 | 89.5% | 90.9% | ||||||||||||||||||||||

| Lackland AFB (San Antonio, Texas) | 8 | 1,060 | 100.0% | 100.0% | ||||||||||||||||||||||

| Navy Support | 21 | 1,243 | 93.9% | 93.9% | ||||||||||||||||||||||

| Redstone Arsenal (Huntsville, Alabama) | 17 | 1,529 | 90.8% | 91.7% | ||||||||||||||||||||||

| Data Center Shells: | ||||||||||||||||||||||||||

| Consolidated Properties | 7 | 1,557 | 100.0% | 100.0% | ||||||||||||||||||||||

| Unconsolidated JV Properties (2) | 19 | 3,182 | 100.0% | 100.0% | ||||||||||||||||||||||

| Total Defense/IT Locations | 176 | 19,409 | 93.2% | 95.0% | ||||||||||||||||||||||

| Regional Office | 8 | 2,144 | 87.3% | 88.9% | ||||||||||||||||||||||

| Core Portfolio | 184 | 21,553 | 92.6% | 94.4% | ||||||||||||||||||||||

| Other Properties | 2 | 157 | 66.2% | 66.2% | ||||||||||||||||||||||

| Total Portfolio | 186 | 21,710 | 92.4% | 94.2% | ||||||||||||||||||||||

| Consolidated Portfolio | 167 | 18,529 | 91.1% | 93.2% | ||||||||||||||||||||||

| As of Period End | ||||||||||||||||||||||||||||||||||||||||||||||||||

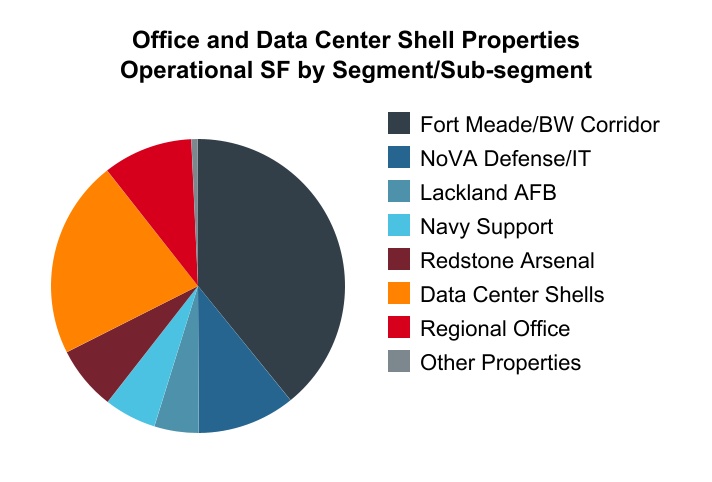

| # of Office and Data Center Shell Properties | Operational Square Feet | % Occupied (1) | % Leased (1) | Annualized Rental Revenue (2) | % of Total Annualized Rental Revenue (2) | NOI from Real Estate Operations | ||||||||||||||||||||||||||||||||||||||||||||

| Property Grouping | Three Months Ended | Year Ended | ||||||||||||||||||||||||||||||||||||||||||||||||

| Core Portfolio: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Same Properties: (3) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Consolidated properties | 148 | 15,728 | 90.8% | 93.1% | $ | 492,848 | 87.0 | % | $ | 72,840 | $ | 298,240 | ||||||||||||||||||||||||||||||||||||||

| Unconsolidated real estate JV | 9 | 1,472 | 100.0% | 100.0% | 2,181 | 0.4 | % | 504 | 2,010 | |||||||||||||||||||||||||||||||||||||||||

| Total Same Properties in Core Portfolio | 157 | 17,200 | 91.6% | 93.7% | 495,029 | 87.3 | % | 73,344 | 300,250 | |||||||||||||||||||||||||||||||||||||||||

| Properties Placed in Service (4) | 17 | 2,643 | 94.8% | 95.3% | 64,192 | 11.3 | % | 12,947 | 41,034 | |||||||||||||||||||||||||||||||||||||||||

| Other unconsolidated JV properties (5) | 10 | 1,710 | 100.0% | 100.0% | 2,379 | 0.4 | % | 573 | 4,429 | |||||||||||||||||||||||||||||||||||||||||

| Total Core Portfolio | 184 | 21,553 | 92.6% | 94.4% | 561,600 | 99.1 | % | 86,864 | 345,713 | |||||||||||||||||||||||||||||||||||||||||

| Wholesale Data Center | N/A | N/A | N/A | N/A | N/A | N/A | 3,074 | 13,066 | ||||||||||||||||||||||||||||||||||||||||||

| Other | 2 | 157 | 66.2% | 66.2% | 5,155 | 0.9 | % | 585 | 2,091 | |||||||||||||||||||||||||||||||||||||||||

| Total Portfolio | 186 | 21,710 | 92.4% | 94.2% | $ | 566,755 | 100.0 | % | $ | 90,523 | $ | 360,870 | ||||||||||||||||||||||||||||||||||||||

| Consolidated Portfolio | 167 | 18,529 | 91.1% | 93.2% | $ | 562,195 | 99.2 | % | $ | 89,444 | $ | 356,841 | ||||||||||||||||||||||||||||||||||||||

| As of Period End | ||||||||||||||||||||||||||||||||||||||||||||||||||

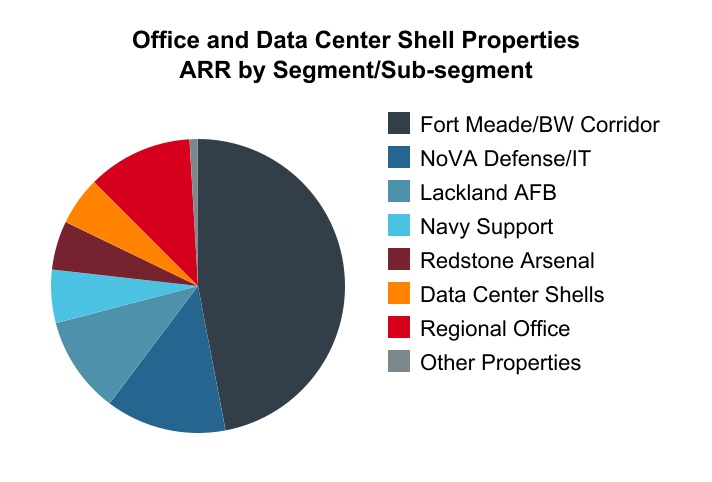

| # of Office and Data Center Shell Properties | Operational Square Feet | % Occupied (1) | % Leased (1) | Annualized Rental Revenue (2) | % of Core Annualized Rental Revenue (2) | NOI from Real Estate Operations | ||||||||||||||||||||||||||||||||||||||||||||

| Property Grouping | Three Months Ended | Year Ended | ||||||||||||||||||||||||||||||||||||||||||||||||

| Core Portfolio: | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations: (6) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Consolidated properties | 157 | 16,227 | 91.9% | 94.0% | $ | 491,361 | 87.5 | % | $ | 78,308 | $ | 307,737 | ||||||||||||||||||||||||||||||||||||||

| Unconsolidated real estate JVs (5) | 19 | 3,182 | 100.0% | 100.0% | 4,560 | 0.8 | % | 1,079 | 4,029 | |||||||||||||||||||||||||||||||||||||||||

| Total Defense/IT Locations | 176 | 19,409 | 93.2% | 95.0% | 495,921 | 88.3 | % | 79,387 | 311,766 | |||||||||||||||||||||||||||||||||||||||||

| Regional Office | 8 | 2,144 | 87.3% | 88.9% | 65,679 | 11.7 | % | 7,477 | 33,947 | |||||||||||||||||||||||||||||||||||||||||

| Total Core Portfolio | 184 | 21,553 | 92.6% | 94.4% | $ | 561,600 | 100.0 | % | $ | 86,864 | $ | 345,713 | ||||||||||||||||||||||||||||||||||||||

| Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||

| Consolidated real estate revenues | |||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations: | |||||||||||||||||||||||||||||||||||||||||

| Fort Meade/BW Corridor | $ | 64,805 | $ | 66,029 | $ | 64,840 | $ | 66,446 | $ | 63,733 | $ | 262,120 | $ | 254,197 | |||||||||||||||||||||||||||

| NoVA Defense/IT | 17,176 | 15,291 | 14,712 | 15,211 | 14,993 | 62,390 | 57,817 | ||||||||||||||||||||||||||||||||||

| Lackland Air Force Base | 16,994 | 14,519 | 13,688 | 12,555 | 13,047 | 57,756 | 50,982 | ||||||||||||||||||||||||||||||||||

| Navy Support | 8,356 | 8,558 | 8,445 | 8,398 | 8,403 | 33,757 | 32,869 | ||||||||||||||||||||||||||||||||||

| Redstone Arsenal | 9,555 | 9,144 | 8,775 | 8,253 | 7,113 | 35,727 | 22,515 | ||||||||||||||||||||||||||||||||||

| Data Center Shells-Consolidated | 7,812 | 6,913 | 8,070 | 8,787 | 8,491 | 31,582 | 29,139 | ||||||||||||||||||||||||||||||||||

| Total Defense/IT Locations | 124,698 | 120,454 | 118,530 | 119,650 | 115,780 | 483,332 | 447,519 | ||||||||||||||||||||||||||||||||||

| Regional Office | 16,199 | 16,810 | 16,884 | 16,677 | 15,092 | 66,570 | 60,627 | ||||||||||||||||||||||||||||||||||

| Wholesale Data Center | 8,235 | 7,717 | 7,204 | 7,334 | 7,421 | 30,490 | 27,011 | ||||||||||||||||||||||||||||||||||

| Other | 1,751 | 1,609 | 1,805 | 1,503 | 1,335 | 6,668 | 3,568 | ||||||||||||||||||||||||||||||||||

| Consolidated real estate revenues | $ | 150,883 | $ | 146,590 | $ | 144,423 | $ | 145,164 | $ | 139,628 | $ | 587,060 | $ | 538,725 | |||||||||||||||||||||||||||

| NOI | |||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations: | |||||||||||||||||||||||||||||||||||||||||

| Fort Meade/BW Corridor | $ | 41,625 | $ | 43,073 | $ | 43,126 | $ | 41,775 | $ | 42,319 | $ | 169,599 | $ | 169,165 | |||||||||||||||||||||||||||

| NoVA Defense/IT | 11,352 | 9,311 | 9,174 | 9,335 | 9,437 | 39,172 | 36,496 | ||||||||||||||||||||||||||||||||||

| Lackland Air Force Base | 7,774 | 7,584 | 6,182 | 5,681 | 5,688 | 27,221 | 21,927 | ||||||||||||||||||||||||||||||||||

| Navy Support | 4,853 | 5,104 | 5,218 | 4,965 | 5,248 | 20,140 | 20,214 | ||||||||||||||||||||||||||||||||||

| Redstone Arsenal | 6,462 | 6,141 | 5,807 | 5,699 | 4,482 | 24,109 | 14,396 | ||||||||||||||||||||||||||||||||||

| Data Center Shells: | |||||||||||||||||||||||||||||||||||||||||

| Consolidated properties | 6,242 | 6,256 | 7,293 | 7,705 | 7,603 | 27,496 | 25,944 | ||||||||||||||||||||||||||||||||||

| COPT’s share of unconsolidated real estate JVs | 1,079 | 1,060 | 973 | 917 | 1,761 | 4,029 | 6,951 | ||||||||||||||||||||||||||||||||||

| Total Defense/IT Locations | 79,387 | 78,529 | 77,773 | 76,077 | 76,538 | 311,766 | 295,093 | ||||||||||||||||||||||||||||||||||

| Regional Office | 7,477 | 8,415 | 9,042 | 9,013 | 8,155 | 33,947 | 31,483 | ||||||||||||||||||||||||||||||||||

| Wholesale Data Center | 3,074 | 3,105 | 3,376 | 3,511 | 4,082 | 13,066 | 13,468 | ||||||||||||||||||||||||||||||||||

| Other | 585 | 411 | 589 | 506 | 529 | 2,091 | 1,792 | ||||||||||||||||||||||||||||||||||

| NOI from real estate operations | $ | 90,523 | $ | 90,460 | $ | 90,780 | $ | 89,107 | $ | 89,304 | $ | 360,870 | $ | 341,836 | |||||||||||||||||||||||||||

| Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||

| Cash NOI | |||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations: | |||||||||||||||||||||||||||||||||||||||||

| Fort Meade/BW Corridor | $ | 42,666 | $ | 42,301 | $ | 42,514 | $ | 39,666 | $ | 42,430 | $ | 167,147 | $ | 167,933 | |||||||||||||||||||||||||||

| NoVA Defense/IT | 9,712 | 9,591 | 9,600 | 9,222 | 9,519 | 38,125 | 37,657 | ||||||||||||||||||||||||||||||||||

| Lackland Air Force Base | 7,793 | 6,637 | 6,122 | 5,999 | 6,006 | 26,551 | 23,539 | ||||||||||||||||||||||||||||||||||

| Navy Support | 4,981 | 5,381 | 5,394 | 4,965 | 5,376 | 20,721 | 20,900 | ||||||||||||||||||||||||||||||||||

| Redstone Arsenal | 5,162 | 5,262 | 4,890 | 4,706 | 4,383 | 20,020 | 12,305 | ||||||||||||||||||||||||||||||||||

| Data Center Shells: | |||||||||||||||||||||||||||||||||||||||||

| Consolidated properties | 5,430 | 5,426 | 6,261 | 6,505 | 6,588 | 23,622 | 22,643 | ||||||||||||||||||||||||||||||||||

| COPT’s share of unconsolidated real estate JVs | 975 | 951 | 871 | 816 | 1,668 | 3,613 | 6,597 | ||||||||||||||||||||||||||||||||||

| Total Defense/IT Locations | 76,719 | 75,549 | 75,652 | 71,879 | 75,970 | 299,799 | 291,574 | ||||||||||||||||||||||||||||||||||

| Regional Office | 6,642 | 7,172 | 7,684 | 7,448 | 8,156 | 28,946 | 30,758 | ||||||||||||||||||||||||||||||||||

| Wholesale Data Center | 3,122 | 3,138 | 3,403 | 3,545 | 4,094 | 13,208 | 13,432 | ||||||||||||||||||||||||||||||||||

| Other | 658 | 447 | 659 | 578 | 582 | 2,342 | 1,830 | ||||||||||||||||||||||||||||||||||

| Cash NOI from real estate operations | 87,141 | 86,306 | 87,398 | 83,450 | 88,802 | 344,295 | 337,594 | ||||||||||||||||||||||||||||||||||

| Straight line rent adjustments and lease incentive amortization | 2,521 | 2,148 | 1,692 | 4,006 | (3,104) | 10,367 | (3,539) | ||||||||||||||||||||||||||||||||||

| Amortization of acquired above- and below-market rents | 100 | 99 | 98 | 99 | 99 | 396 | 390 | ||||||||||||||||||||||||||||||||||

| Amortization of intangibles and other assets to property operating expenses | (139) | (140) | (139) | (139) | (122) | (557) | (227) | ||||||||||||||||||||||||||||||||||

| Lease termination fees, net | (893) | 853 | 1,094 | 1,362 | 141 | 2,416 | 832 | ||||||||||||||||||||||||||||||||||

| Tenant funded landlord assets and lease incentives | 1,689 | 1,085 | 535 | 228 | 3,395 | 3,537 | 6,432 | ||||||||||||||||||||||||||||||||||

| Cash NOI adjustments in unconsolidated real estate JVs | 104 | 109 | 102 | 101 | 93 | 416 | 354 | ||||||||||||||||||||||||||||||||||

| NOI from real estate operations | $ | 90,523 | $ | 90,460 | $ | 90,780 | $ | 89,107 | $ | 89,304 | $ | 360,870 | $ | 341,836 | |||||||||||||||||||||||||||

| # of Properties | Operational Square Feet | Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||||||||||||||

| Core Portfolio: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fort Meade/BW Corridor | 87 | 8,187 | 90.1 | % | 89.6 | % | 90.4 | % | 90.3 | % | 91.2 | % | 90.1 | % | 91.4 | % | |||||||||||||||||||||||||||||||||||||

| NoVA Defense/IT | 13 | 1,988 | 87.8 | % | 86.9 | % | 87.7 | % | 87.8 | % | 88.4 | % | 87.6 | % | 86.9 | % | |||||||||||||||||||||||||||||||||||||

| Lackland Air Force Base | 7 | 953 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||||||||||||||||||||||||||||||

| Navy Support | 21 | 1,243 | 95.1 | % | 96.7 | % | 96.9 | % | 96.8 | % | 96.9 | % | 96.4 | % | 94.8 | % | |||||||||||||||||||||||||||||||||||||

| Redstone Arsenal | 10 | 806 | 93.7 | % | 99.0 | % | 99.2 | % | 99.2 | % | 99.1 | % | 97.8 | % | 99.5 | % | |||||||||||||||||||||||||||||||||||||

| Data Center Shells: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Consolidated properties | 3 | 594 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||||||||||||||||||||||||||||||

| Unconsolidated JV properties | 9 | 1,472 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||||||||||||||||||||||||||||||

| Total Defense/IT Locations | 150 | 15,243 | 92.4 | % | 92.4 | % | 93.0 | % | 92.9 | % | 93.4 | % | 92.7 | % | 93.2 | % | |||||||||||||||||||||||||||||||||||||

| Regional Office | 7 | 1,957 | 90.6 | % | 90.8 | % | 92.0 | % | 92.0 | % | 92.1 | % | 91.4 | % | 91.7 | % | |||||||||||||||||||||||||||||||||||||

| Core Portfolio Same Properties | 157 | 17,200 | 92.2 | % | 92.2 | % | 92.8 | % | 92.8 | % | 93.3 | % | 92.5 | % | 93.0 | % | |||||||||||||||||||||||||||||||||||||

| Other Same Properties | 2 | 157 | 66.2 | % | 66.2 | % | 67.0 | % | 68.4 | % | 68.4 | % | 67.0 | % | 67.5 | % | |||||||||||||||||||||||||||||||||||||

| Total Same Properties | 159 | 17,357 | 91.9 | % | 92.0 | % | 92.6 | % | 92.6 | % | 93.0 | % | 92.3 | % | 92.8 | % | |||||||||||||||||||||||||||||||||||||

Same Properties (1) Period End Occupancy Rates by Segment (square feet in thousands) | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| # of Properties | Operational Square Feet | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Core Portfolio: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fort Meade/BW Corridor | 87 | 8,187 | 90.1 | % | 90.1 | % | 89.8 | % | 90.3 | % | 91.0 | % | |||||||||||||||||||||||||||||||||||||||||

| NoVA Defense/IT | 13 | 1,988 | 87.7 | % | 86.8 | % | 87.7 | % | 87.6 | % | 88.1 | % | |||||||||||||||||||||||||||||||||||||||||

| Lackland Air Force Base | 7 | 953 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||||||||||||||||||||||||||||||||||

| Navy Support | 21 | 1,243 | 93.9 | % | 96.5 | % | 96.9 | % | 96.9 | % | 97.2 | % | |||||||||||||||||||||||||||||||||||||||||

| Redstone Arsenal | 10 | 806 | 83.7 | % | 98.7 | % | 99.2 | % | 99.2 | % | 98.9 | % | |||||||||||||||||||||||||||||||||||||||||

| Data Center Shells: | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Consolidated properties | 3 | 594 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||||||||||||||||||||||||||||||||||

| Unconsolidated JV properties | 9 | 1,472 | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | 100.0 | % | |||||||||||||||||||||||||||||||||||||||||

| Total Defense/IT Locations | 150 | 15,243 | 91.7 | % | 92.6 | % | 92.6 | % | 92.9 | % | 93.3 | % | |||||||||||||||||||||||||||||||||||||||||

| Regional Office | 7 | 1,957 | 90.2 | % | 90.8 | % | 91.3 | % | 92.5 | % | 92.1 | % | |||||||||||||||||||||||||||||||||||||||||

| Core Portfolio Same Properties | 157 | 17,200 | 91.6 | % | 92.4 | % | 92.5 | % | 92.8 | % | 93.2 | % | |||||||||||||||||||||||||||||||||||||||||

| Other Same Properties | 2 | 157 | 66.2 | % | 66.2 | % | 66.2 | % | 68.4 | % | 68.4 | % | |||||||||||||||||||||||||||||||||||||||||

| Total Same Properties | 159 | 17,357 | 91.3 | % | 92.2 | % | 92.2 | % | 92.6 | % | 92.9 | % | |||||||||||||||||||||||||||||||||||||||||

| Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||

| Same Properties real estate revenues | |||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations: | |||||||||||||||||||||||||||||||||||||||||

| Fort Meade/BW Corridor | $ | 62,347 | $ | 64,643 | $ | 63,669 | $ | 65,278 | $ | 62,912 | $ | 255,937 | $ | 251,479 | |||||||||||||||||||||||||||

| NoVA Defense/IT | 15,081 | 15,266 | 14,713 | 15,127 | 14,993 | 60,187 | 57,816 | ||||||||||||||||||||||||||||||||||

| Lackland Air Force Base | 15,951 | 13,551 | 13,420 | 12,555 | 13,047 | 55,477 | 50,983 | ||||||||||||||||||||||||||||||||||

| Navy Support | 8,356 | 8,558 | 8,445 | 8,398 | 8,403 | 33,757 | 32,869 | ||||||||||||||||||||||||||||||||||

| Redstone Arsenal | 4,781 | 4,828 | 4,785 | 4,555 | 4,487 | 18,949 | 18,017 | ||||||||||||||||||||||||||||||||||

| Data Center Shells-Consolidated | 2,656 | 2,361 | 2,366 | 2,419 | 2,559 | 9,802 | 9,466 | ||||||||||||||||||||||||||||||||||

| Total Defense/IT Locations | 109,172 | 109,207 | 107,398 | 108,332 | 106,401 | 434,109 | 420,630 | ||||||||||||||||||||||||||||||||||

| Regional Office | 14,470 | 15,121 | 15,205 | 14,995 | 14,829 | 59,791 | 60,364 | ||||||||||||||||||||||||||||||||||

| Other Properties | 666 | 665 | 652 | 665 | 663 | 2,648 | 2,790 | ||||||||||||||||||||||||||||||||||

| Same Properties real estate revenues | $ | 124,308 | $ | 124,993 | $ | 123,255 | $ | 123,992 | $ | 121,893 | $ | 496,548 | $ | 483,784 | |||||||||||||||||||||||||||

| Same Properties NOI | |||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations: | |||||||||||||||||||||||||||||||||||||||||

| Fort Meade/BW Corridor | $ | 39,588 | $ | 42,032 | $ | 42,378 | $ | 40,975 | $ | 41,756 | $ | 164,973 | $ | 167,328 | |||||||||||||||||||||||||||

| NoVA Defense/IT | 9,667 | 9,288 | 9,174 | 9,251 | 9,436 | 37,380 | 36,496 | ||||||||||||||||||||||||||||||||||

| Lackland Air Force Base | 6,769 | 6,653 | 5,924 | 5,682 | 5,688 | 25,028 | 21,927 | ||||||||||||||||||||||||||||||||||

| Navy Support | 4,853 | 5,104 | 5,218 | 4,965 | 5,248 | 20,140 | 20,214 | ||||||||||||||||||||||||||||||||||

| Redstone Arsenal | 2,963 | 3,015 | 2,951 | 2,912 | 2,684 | 11,841 | 11,091 | ||||||||||||||||||||||||||||||||||

| Data Center Shells: | |||||||||||||||||||||||||||||||||||||||||

| Consolidated properties | 2,059 | 2,068 | 2,070 | 2,066 | 2,072 | 8,263 | 7,890 | ||||||||||||||||||||||||||||||||||

| COPT’s share of unconsolidated real estate JV | 504 | 504 | 503 | 499 | 506 | 2,010 | 2,021 | ||||||||||||||||||||||||||||||||||

| Total Defense/IT Locations | 66,403 | 68,664 | 68,218 | 66,350 | 67,390 | 269,635 | 266,967 | ||||||||||||||||||||||||||||||||||

| Regional Office | 6,941 | 7,739 | 8,220 | 7,715 | 7,892 | 30,615 | 31,220 | ||||||||||||||||||||||||||||||||||

| Other Properties | 347 | 325 | 381 | 304 | 351 | 1,357 | 1,643 | ||||||||||||||||||||||||||||||||||

| Same Properties NOI | $ | 73,691 | $ | 76,728 | $ | 76,819 | $ | 74,369 | $ | 75,633 | $ | 301,607 | $ | 299,830 | |||||||||||||||||||||||||||

| Three Months Ended | Years Ended | ||||||||||||||||||||||||||||||||||||||||

| 12/31/21 | 9/30/21 | 6/30/21 | 3/31/21 | 12/31/20 | 12/31/21 | 12/31/20 | |||||||||||||||||||||||||||||||||||

| Same Properties cash NOI | |||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations: | |||||||||||||||||||||||||||||||||||||||||

| Fort Meade/BW Corridor | $ | 41,422 | $ | 41,706 | $ | 42,074 | $ | 39,192 | $ | 42,069 | $ | 164,394 | $ | 166,969 | |||||||||||||||||||||||||||

| NoVA Defense/IT | 10,121 | 9,593 | 9,599 | 9,138 | 9,519 | 38,451 | 37,657 | ||||||||||||||||||||||||||||||||||

| Lackland Air Force Base | 6,870 | 6,664 | 6,133 | 5,999 | 6,005 | 25,666 | 23,539 | ||||||||||||||||||||||||||||||||||

| Navy Support | 4,982 | 5,381 | 5,394 | 4,965 | 5,376 | 20,722 | 20,900 | ||||||||||||||||||||||||||||||||||

| Redstone Arsenal | 3,064 | 3,111 | 3,054 | 2,957 | 2,790 | 12,186 | 10,521 | ||||||||||||||||||||||||||||||||||

| Data Center Shells: | |||||||||||||||||||||||||||||||||||||||||

| Consolidated properties | 1,816 | 1,823 | 1,778 | 1,806 | 1,783 | 7,223 | 6,760 | ||||||||||||||||||||||||||||||||||

| COPT’s share of unconsolidated real estate JV | 469 | 465 | 465 | 456 | 460 | 1,855 | 1,825 | ||||||||||||||||||||||||||||||||||

| Total Defense/IT Locations | 68,744 | 68,743 | 68,497 | 64,513 | 68,002 | 270,497 | 268,171 | ||||||||||||||||||||||||||||||||||

| Regional Office | 7,762 | 8,176 | 8,540 | 7,832 | 8,157 | 32,310 | 30,759 | ||||||||||||||||||||||||||||||||||

| Other Properties | 360 | 300 | 392 | 319 | 356 | 1,371 | 1,609 | ||||||||||||||||||||||||||||||||||

| Same Properties cash NOI | 76,866 | 77,219 | 77,429 | 72,664 | 76,515 | 304,178 | 300,539 | ||||||||||||||||||||||||||||||||||

| Straight line rent adjustments and lease incentive amortization | (2,604) | (1,671) | (2,283) | 24 | (1,416) | (6,534) | (2,998) | ||||||||||||||||||||||||||||||||||

| Amortization of acquired above- and below-market rents | 100 | 99 | 98 | 99 | 99 | 396 | 390 | ||||||||||||||||||||||||||||||||||

| Amortization of intangibles and other assets to property operating expenses | — | — | — | — | — | — | (69) | ||||||||||||||||||||||||||||||||||

| Lease termination fees, net | (893) | 853 | 1,094 | 1,362 | 141 | 2,416 | 834 | ||||||||||||||||||||||||||||||||||

| Tenant funded landlord assets and lease incentives | 187 | 191 | 441 | 178 | 249 | 997 | 939 | ||||||||||||||||||||||||||||||||||

| Cash NOI adjustments in unconsolidated real estate JV | 35 | 37 | 40 | 42 | 45 | 154 | 195 | ||||||||||||||||||||||||||||||||||

| Same Properties NOI | $ | 73,691 | $ | 76,728 | $ | 76,819 | $ | 74,369 | $ | 75,633 | $ | 301,607 | $ | 299,830 | |||||||||||||||||||||||||||

| Percentage change in total Same Properties cash NOI (1) | 0.5% | 1.2% | |||||||||||||||||||||||||||||||||||||||

| Percentage change in Defense/IT Locations Same Properties cash NOI (1) | 1.1% | 0.9% | |||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations | |||||||||||||||||||||||||||||||||||||||||||||||

| Ft Meade/BW Corridor | NoVA Defense/IT | Navy Support | Redstone Arsenal | Total Defense/IT Locations | Regional Office | Other | Total | ||||||||||||||||||||||||||||||||||||||||

| Renewed Space | |||||||||||||||||||||||||||||||||||||||||||||||

| Leased Square Feet | 312 | 56 | 78 | — | 446 | 222 | 33 | 701 | |||||||||||||||||||||||||||||||||||||||

| Expiring Square Feet | 331 | 56 | 132 | 121 | 640 | 281 | 33 | 954 | |||||||||||||||||||||||||||||||||||||||

| Vacating Square Feet | 19 | — | 55 | 121 | 194 | 59 | — | 254 | |||||||||||||||||||||||||||||||||||||||

| Retention Rate (% based upon square feet) | 94.3 | % | 100.0 | % | 58.8 | % | — | % | 69.6 | % | 79.0 | % | 100.0 | % | 73.4 | % | |||||||||||||||||||||||||||||||

| Statistics for Completed Leasing: | |||||||||||||||||||||||||||||||||||||||||||||||

| Per Annum Average Committed Cost per Square Foot | $ | 1.95 | $ | 4.57 | $ | 2.49 | $ | — | $ | 2.37 | $ | 7.62 | $ | 0.86 | $ | 3.97 | |||||||||||||||||||||||||||||||

| Weighted Average Lease Term in Years | 7.5 | 3.6 | 2.9 | — | 6.2 | 13.9 | 1.8 | 8.5 | |||||||||||||||||||||||||||||||||||||||

| Straight-line Rent Per Square Foot | |||||||||||||||||||||||||||||||||||||||||||||||

| Renewal Straight-line Rent | $ | 37.76 | $ | 36.46 | $ | 19.53 | $ | — | $ | 34.41 | $ | 34.89 | $ | 21.53 | $ | 33.96 | |||||||||||||||||||||||||||||||

| Expiring Straight-line Rent | $ | 34.93 | $ | 35.08 | $ | 20.06 | $ | — | $ | 32.35 | $ | 36.03 | $ | 21.20 | $ | 33.00 | |||||||||||||||||||||||||||||||

| Change in Straight-line Rent | 8.1 | % | 3.9 | % | (2.6) | % | — | % | 6.4 | % | (3.1) | % | 1.6 | % | 2.9 | % | |||||||||||||||||||||||||||||||

| Cash Rent Per Square Foot | |||||||||||||||||||||||||||||||||||||||||||||||

| Renewal Cash Rent | $ | 36.15 | $ | 35.32 | $ | 21.18 | $ | — | $ | 33.43 | $ | 33.20 | $ | 21.11 | $ | 32.78 | |||||||||||||||||||||||||||||||

| Expiring Cash Rent | $ | 36.42 | $ | 38.50 | $ | 20.58 | $ | — | $ | 33.92 | $ | 38.36 | $ | 22.37 | $ | 34.79 | |||||||||||||||||||||||||||||||

| Change in Cash Rent | (0.8) | % | (8.3) | % | 2.9 | % | — | % | (1.4) | % | (13.5) | % | (5.7) | % | (5.8) | % | |||||||||||||||||||||||||||||||

| Average Escalations Per Year | 2.3 | % | 2.5 | % | 2.6 | % | — | % | 2.4 | % | 2.3 | % | 4.7 | % | 2.3 | % | |||||||||||||||||||||||||||||||

| New Leases | |||||||||||||||||||||||||||||||||||||||||||||||

| Development and Redevelopment Space | |||||||||||||||||||||||||||||||||||||||||||||||

| Leased Square Feet | — | — | — | 263 | 263 | — | — | 263 | |||||||||||||||||||||||||||||||||||||||

| Statistics for Completed Leasing: | |||||||||||||||||||||||||||||||||||||||||||||||

| Per Annum Average Committed Cost per Square Foot | $ | — | $ | — | $ | — | $ | 7.09 | $ | 7.09 | $ | — | $ | — | $ | 7.09 | |||||||||||||||||||||||||||||||

| Weighted Average Lease Term in Years | — | — | — | 11.0 | 11.0 | — | — | 11.0 | |||||||||||||||||||||||||||||||||||||||

| Straight-line Rent Per Square Foot | $ | — | $ | — | $ | — | $ | 29.99 | $ | 29.99 | $ | — | $ | — | $ | 29.99 | |||||||||||||||||||||||||||||||

| Cash Rent Per Square Foot | $ | — | $ | — | $ | — | $ | 28.99 | $ | 28.99 | $ | — | $ | — | $ | 28.99 | |||||||||||||||||||||||||||||||

| Vacant Space | |||||||||||||||||||||||||||||||||||||||||||||||

| Leased Square Feet | 158 | 11 | 11 | 4 | 185 | 11 | — | 196 | |||||||||||||||||||||||||||||||||||||||

| Statistics for Completed Leasing: | |||||||||||||||||||||||||||||||||||||||||||||||

| Per Annum Average Committed Cost per Square Foot | $ | 8.49 | $ | 13.21 | $ | 5.64 | $ | 4.49 | $ | 8.52 | $ | 10.09 | $ | — | $ | 8.61 | |||||||||||||||||||||||||||||||

| Weighted Average Lease Term in Years | 8.0 | 5.0 | 4.2 | 3.0 | 7.4 | 8.4 | — | 7.5 | |||||||||||||||||||||||||||||||||||||||

| Straight-line Rent Per Square Foot | $ | 24.33 | $ | 36.27 | $ | 25.77 | $ | 29.00 | $ | 25.26 | $ | 31.53 | $ | — | $ | 25.62 | |||||||||||||||||||||||||||||||

| Cash Rent Per Square Foot | $ | 23.14 | $ | 34.50 | $ | 26.77 | $ | 28.50 | $ | 24.19 | $ | 30.73 | $ | — | $ | 24.56 | |||||||||||||||||||||||||||||||

| Total Square Feet Leased | 470 | 67 | 89 | 267 | 894 | 233 | 33 | 1,160 | |||||||||||||||||||||||||||||||||||||||

| Average Escalations Per Year | 2.9 | % | 2.5 | % | 2.6 | % | 2.5 | % | 2.7 | % | 2.3 | % | 4.7 | % | 2.6 | % | |||||||||||||||||||||||||||||||

| Average Escalations Excl. Data Center Shells | 2.6 | % | |||||||||||||||||||||||||||||||||||||||||||||

| Defense/IT Locations | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Ft Meade/BW Corridor | NoVA Defense/IT | Lackland Air Force Base | Navy Support | Redstone Arsenal | Data Center Shells | Total Defense/IT Locations | Regional Office | Other | Total | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Renewed Space | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Leased Square Feet | 899 | 122 | 250 | 269 | 252 | — | 1,792 | 237 | 40 | 2,068 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Expiring Square Feet | 1,224 | 166 | 250 | 353 | 378 | — | 2,370 | 375 | 43 | 2,789 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Vacating Square Feet | 325 | 44 | — | 84 | 125 | — | 579 | 138 | 3 | 720 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Retention Rate (% based upon square feet) | 73.4 | % | 73.5 | % | 100.0 | % | 76.1 | % | 66.8 | % | — | % | 75.6 | % | 63.2 | % | 92.0 | % | 74.2 | % | |||||||||||||||||||||||||||||||||||||||

| Statistics for Completed Leasing: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Per Annum Average Committed Cost per Square Foot | $ | 3.26 | $ | 3.31 | $ | 2.00 | $ | 1.85 | $ | 0.48 | $ | — | $ | 2.48 | $ | 7.21 | $ | 0.76 | $ | 2.99 | |||||||||||||||||||||||||||||||||||||||

| Weighted Average Lease Term in Years | 5.7 | 4.0 | 5.0 | 3.0 | 1.0 | — | 4.4 | 13.1 | 3.6 | 5.4 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Straight-line Rent Per Square Foot | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Renewal Straight-line Rent | $ | 36.20 | $ | 33.54 | $ | 50.29 | $ | 21.45 | $ | 23.65 | $ | — | $ | 34.00 | $ | 34.81 | $ | 22.29 | $ | 33.87 | |||||||||||||||||||||||||||||||||||||||

| Expiring Straight-line Rent | $ | 34.29 | $ | 32.08 | $ | 44.30 | $ | 20.98 | $ | 22.93 | $ | — | $ | 31.94 | $ | 35.85 | $ | 21.11 | $ | 32.18 | |||||||||||||||||||||||||||||||||||||||

| Change in Straight-line Rent | 5.5 | % | 4.6 | % | 13.5 | % | 2.3 | % | 3.1 | % | — | % | 6.5 | % | (2.9) | % | 5.6 | % | 5.2 | % | |||||||||||||||||||||||||||||||||||||||

| Cash Rent Per Square Foot | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Renewal Cash Rent | $ | 35.65 | $ | 34.36 | $ | 48.52 | $ | 21.90 | $ | 23.65 | $ | — | $ | 33.61 | $ | 33.24 | $ | 22.03 | $ | 33.34 | |||||||||||||||||||||||||||||||||||||||

| Expiring Cash Rent | $ | 36.25 | $ | 36.01 | $ | 47.70 | $ | 21.92 | $ | 23.08 | $ | — | $ | 33.83 | $ | 38.07 | $ | 22.41 | $ | 34.09 | |||||||||||||||||||||||||||||||||||||||

| Change in Cash Rent | (1.7) | % | (4.6) | % | 1.7 | % | (0.1) | % | 2.5 | % | — | % | (0.7) | % | (12.7) | % | (1.7) | % | (2.2) | % | |||||||||||||||||||||||||||||||||||||||

| Average Escalations Per Year | 2.2 | % | 2.5 | % | 3.0 | % | 2.6 | % | — | % | — | % | 2.4 | % | 2.3 | % | 1.9 | % | 2.3 | % | |||||||||||||||||||||||||||||||||||||||

| New Leases | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Development and Redevelopment Space | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Leased Square Feet | 183 | — | — | — | 727 | 265 | 1,174 | 3 | — | 1,178 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Statistics for Completed Leasing: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Per Annum Average Committed Cost per Square Foot | $ | 8.91 | $ | — | $ | — | $ | — | $ | 6.92 | $ | — | $ | 5.67 | $ | 13.83 | $ | — | $ | 5.69 | |||||||||||||||||||||||||||||||||||||||

| Weighted Average Lease Term in Years | 11.8 | — | — | — | 13.2 | 15.0 | 13.4 | 10.0 | — | 13.4 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Straight-line Rent Per Square Foot | $ | 37.87 | $ | — | $ | — | $ | — | $ | 29.01 | $ | 31.40 | $ | 30.93 | $ | 73.66 | $ | — | $ | 31.05 | |||||||||||||||||||||||||||||||||||||||

| Cash Rent Per Square Foot | $ | 38.00 | $ | — | $ | — | $ | — | $ | 27.50 | $ | 27.70 | $ | 29.18 | $ | 68.89 | $ | — | $ | 29.29 | |||||||||||||||||||||||||||||||||||||||

| Vacant Space | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Leased Square Feet | 501 | 63 | — | 18 | 9 | — | 592 | 24 | — | 616 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Statistics for Completed Leasing: | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Per Annum Average Committed Cost per Square Foot | $ | 8.86 | $ | 7.89 | $ | — | $ | 5.81 | $ | 3.07 | $ | — | $ | 8.58 | $ | 9.27 | $ | — | $ | 8.60 | |||||||||||||||||||||||||||||||||||||||

| Weighted Average Lease Term in Years | 8.5 | 6.7 | — | 5.9 | 4.2 | — | 8.2 | 9.0 | — | 8.2 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Straight-line Rent Per Square Foot | $ | 26.88 | $ | 31.08 | $ | — | $ | 30.92 | $ | 26.40 | $ | — | $ | 27.44 | $ | 30.48 | $ | — | $ | 27.56 | |||||||||||||||||||||||||||||||||||||||

| Cash Rent Per Square Foot | $ | 26.13 | $ | 30.96 | $ | — | $ | 32.93 | $ | 26.15 | $ | — | $ | 26.85 | $ | 29.41 | $ | — | $ | 26.95 | |||||||||||||||||||||||||||||||||||||||

| Total Square Feet Leased | 1,583 | 185 | 250 | 286 | 988 | 265 | 3,558 | 265 | 40 | 3,862 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Average Escalations Per Year | 2.5 | % | 2.5 | % | 3.0 | % | 2.6 | % | 2.5 | % | 2.0 | % | 2.5 | % | 2.3 | % | 1.9 | % | 2.4 | % | |||||||||||||||||||||||||||||||||||||||

| Average Escalations Excl. Data Center Shells | 2.5 | % | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Segment of Lease and Year of Expiration (2) | Square Footage of Leases Expiring | Annualized Rental Revenue of Expiring Leases (3) | % of Core/Total Annualized Rental Revenue Expiring (3)(4) | Annualized Rental Revenue of Expiring Leases per Occupied Sq. Foot (3) | ||||||||||||||||||||||

| Core Portfolio | ||||||||||||||||||||||||||

| Ft Meade/BW Corridor | 978 | $ | 32,788 | 5.8 | % | $ | 33.58 | |||||||||||||||||||

| NoVA Defense/IT | 42 | 1,254 | 0.2 | % | 30.09 | |||||||||||||||||||||

| Navy Support | 201 | 5,723 | 1.0 | % | 28.19 | |||||||||||||||||||||

| Redstone Arsenal | 88 | 2,119 | 0.4 | % | 23.98 | |||||||||||||||||||||

| Regional Office | 327 | 11,136 | 2.0 | % | 33.87 | |||||||||||||||||||||

| 2022 | 1,636 | 53,020 | 9.4 | % | 32.36 | |||||||||||||||||||||

| Ft Meade/BW Corridor | 1,337 | 50,328 | 9.0 | % | 37.62 | |||||||||||||||||||||

| NoVA Defense/IT | 115 | 3,639 | 0.6 | % | 31.67 | |||||||||||||||||||||

| Navy Support | 274 | 7,269 | 1.3 | % | 26.52 | |||||||||||||||||||||

| Redstone Arsenal | 207 | 4,775 | 0.9 | % | 23.04 | |||||||||||||||||||||

| Regional Office | 188 | 4,599 | 0.8 | % | 24.45 | |||||||||||||||||||||

| 2023 | 2,121 | 70,611 | 12.6 | % | 33.27 | |||||||||||||||||||||

| Ft Meade/BW Corridor | 1,128 | 41,808 | 7.4 | % | 37.04 | |||||||||||||||||||||

| NoVA Defense/IT | 479 | 17,164 | 3.1 | % | 35.86 | |||||||||||||||||||||

| Navy Support | 307 | 7,448 | 1.3 | % | 24.27 | |||||||||||||||||||||

| Redstone Arsenal | 75 | 1,861 | 0.3 | % | 24.69 | |||||||||||||||||||||

| Data Center Shells-Unconsolidated JV Properties | 546 | 669 | 0.1 | % | 12.25 | |||||||||||||||||||||

| Regional Office | 78 | 2,393 | 0.4 | % | 30.27 | |||||||||||||||||||||

| 2024 | 2,613 | 71,343 | 12.7 | % | 33.60 | |||||||||||||||||||||

| Ft Meade/BW Corridor | 1,727 | 61,058 | 10.9 | % | 35.30 | |||||||||||||||||||||

| NoVA Defense/IT | 286 | 11,889 | 2.1 | % | 41.56 | |||||||||||||||||||||

| Lackland Air Force Base | 703 | 39,605 | 7.1 | % | 56.36 | |||||||||||||||||||||

| Navy Support | 98 | 1,882 | 0.3 | % | 19.20 | |||||||||||||||||||||

| Redstone Arsenal | 253 | 5,364 | 1.0 | % | 21.07 | |||||||||||||||||||||

| Data Center Shells-Unconsolidated JV Properties | 121 | 156 | — | % | 12.93 | |||||||||||||||||||||

| Regional Office | 105 | 3,979 | 0.7 | % | 37.99 | |||||||||||||||||||||

| 2025 | 3,293 | 123,933 | 22.1 | % | 38.89 | |||||||||||||||||||||

| Ft Meade/BW Corridor | 687 | 26,651 | 4.7 | % | 38.79 | |||||||||||||||||||||

| NoVA Defense/IT | 34 | 1,025 | 0.2 | % | 30.07 | |||||||||||||||||||||

| Lackland Air Force Base | 250 | 12,130 | 2.2 | % | 48.52 | |||||||||||||||||||||

| Navy Support | 119 | 3,963 | 0.7 | % | 33.13 | |||||||||||||||||||||

| Redstone Arsenal | 18 | 402 | 0.1 | % | 22.91 | |||||||||||||||||||||

| Data Center Shells-Unconsolidated JV Properties | 446 | 740 | 0.1 | % | 16.61 | |||||||||||||||||||||

| Regional Office | 235 | 7,849 | 1.4 | % | 33.47 | |||||||||||||||||||||

| 2026 | 1,789 | 52,760 | 9.4 | % | 38.03 | |||||||||||||||||||||

| Thereafter | ||||||||||||||||||||||||||

| Consolidated Properties | 6,445 | 186,938 | 33.4 | % | 28.20 | |||||||||||||||||||||

| Unconsolidated JV Properties | 2,069 | 2,995 | 0.5 | % | 14.47 | |||||||||||||||||||||

| Core Portfolio | 19,966 | $ | 561,600 | 100.0 | % | $ | 32.52 | |||||||||||||||||||

| Segment of Lease and Year of Expiration (2) | Square Footage of Leases Expiring | Annualized Rental Revenue of Expiring Leases (3) | % of Core/Total Annualized Rental Revenue Expiring (3)(4) | Annualized Rental Revenue of Expiring Leases per Occupied Sq. Foot (3) | ||||||||||||||||||||||

| Core Portfolio | 19,966 | $ | 561,600 | 99.1 | % | $ | 32.52 | |||||||||||||||||||

| Other | 104 | 5,155 | 0.9 | % | 24.10 | |||||||||||||||||||||

| Total Portfolio | 20,070 | $ | 566,755 | 100.0 | % | $ | 32.47 | |||||||||||||||||||

| Consolidated Portfolio | 16,888 | $ | 562,195 | |||||||||||||||||||||||

| Unconsolidated JV Properties | 3,182 | $ | 4,560 | |||||||||||||||||||||||

| Segment of Lease and Quarter of Expiration (2) | Square Footage of Leases Expiring | Annualized Rental Revenue of Expiring Leases (3) | % of Core Annualized Rental Revenue Expiring (3) | Annualized Rental Revenue of Expiring Leases per Occupied Sq. Foot | ||||||||||||||||||||||

| Core Portfolio | ||||||||||||||||||||||||||

| Ft Meade/BW Corridor | 237 | $ | 6,705 | 1.2 | % | $ | 28.31 | |||||||||||||||||||

| NoVA Defense/IT | 11 | 262 | — | % | 22.86 | |||||||||||||||||||||

| Navy Support | 71 | 1,913 | 0.3 | % | 26.82 | |||||||||||||||||||||

| Regional Office | 182 | 6,117 | 1.1 | % | 33.51 | |||||||||||||||||||||

| Q1 2022 | 501 | 14,997 | 2.6 | % | 29.88 | |||||||||||||||||||||

| Ft Meade/BW Corridor | 171 | 5,113 | 0.9 | % | 29.86 | |||||||||||||||||||||

| NoVA Defense/IT | 15 | 506 | 0.1 | % | 32.84 | |||||||||||||||||||||

| Navy Support | 20 | 1,119 | 0.2 | % | 55.60 | |||||||||||||||||||||

| Redstone Arsenal | 49 | 1,124 | 0.2 | % | 23.01 | |||||||||||||||||||||

| Regional Office | 45 | 1,654 | 0.3 | % | 36.72 | |||||||||||||||||||||

| Q2 2022 | 300 | 9,516 | 1.7 | % | 31.65 | |||||||||||||||||||||

| Ft Meade/BW Corridor | 247 | 9,099 | 1.6 | % | 36.73 | |||||||||||||||||||||

| Navy Support | 75 | 1,805 | 0.3 | % | 24.16 | |||||||||||||||||||||

| Redstone Arsenal | 10 | 281 | 0.1 | % | 27.32 | |||||||||||||||||||||

| Regional Office | 20 | 676 | 0.1 | % | 33.38 | |||||||||||||||||||||

| Q3 2022 | 352 | 11,861 | 2.1 | % | 33.60 | |||||||||||||||||||||

| Ft Meade/BW Corridor | 323 | 11,872 | 2.1 | % | 36.75 | |||||||||||||||||||||

| NoVA Defense/IT | 15 | 486 | 0.1 | % | 32.83 | |||||||||||||||||||||

| Navy Support | 35 | 886 | 0.2 | % | 25.56 | |||||||||||||||||||||

| Redstone Arsenal | 29 | 714 | 0.1 | % | 24.43 | |||||||||||||||||||||

| Regional Office | 81 | 2,688 | 0.5 | % | 33.22 | |||||||||||||||||||||

| Q4 2022 | 483 | 16,646 | 3.0 | % | 34.49 | |||||||||||||||||||||

| 1,636 | $ | 53,020 | 9.4 | % | $ | 32.36 | ||||||||||||||||||||

| Tenant | Total Annualized Rental Revenue (2) | % of Total Annualized Rental Revenue (2) | Occupied Square Feet in Office and Data Center Shells | Weighted Average Remaining Lease Term in Office and Data Center Shells (3) | |||||||||||||||||||||||||

| United States Government | (4) | $ | 209,830 | 35.6 | % | 5,042 | 4.5 | ||||||||||||||||||||||

| Fortune 100 Company | 54,512 | 9.2 | % | 4,983 | 8.6 | ||||||||||||||||||||||||

| General Dynamics Corporation | 33,224 | 5.6 | % | 752 | 2.2 | ||||||||||||||||||||||||

| The Boeing Company | 14,910 | 2.5 | % | 489 | 2.1 | ||||||||||||||||||||||||

| CACI International Inc | 13,861 | 2.4 | % | 354 | 3.2 | ||||||||||||||||||||||||

| Peraton Corp. | 12,433 | 2.1 | % | 349 | 6.3 | ||||||||||||||||||||||||

| Booz Allen Hamilton, Inc. | 11,125 | 1.9 | % | 297 | 3.3 | ||||||||||||||||||||||||

| CareFirst Inc. | 10,312 | 1.7 | % | 312 | 10.3 | ||||||||||||||||||||||||

| Northrop Grumman Corporation | 8,220 | 1.4 | % | 284 | 1.9 | ||||||||||||||||||||||||

| Raytheon Technologies Corporation | 6,684 | 1.1 | % | 202 | 2.1 | ||||||||||||||||||||||||

| Wells Fargo & Company | 6,510 | 1.1 | % | 159 | 6.7 | ||||||||||||||||||||||||

| Yulista Holding, LLC | 6,494 | 1.1 | % | 366 | 8.0 | ||||||||||||||||||||||||

| AT&T Corporation | 6,304 | 1.1 | % | 321 | 7.8 | ||||||||||||||||||||||||

| Miles and Stockbridge, PC | 6,180 | 1.0 | % | 160 | 5.7 | ||||||||||||||||||||||||

| Mantech International Corp. | 5,931 | 1.0 | % | 195 | 3.0 | ||||||||||||||||||||||||

| Morrison & Foerster, LLP | 5,925 | 1.0 | % | 102 | 15.3 | ||||||||||||||||||||||||

| Jacobs Engineering Group Inc. | 5,734 | 1.0 | % | 177 | 7.0 | ||||||||||||||||||||||||

| Transamerica Life Insurance Company | 5,296 | 0.9 | % | 140 | — | ||||||||||||||||||||||||

| The MITRE Corporation | 4,932 | 0.8 | % | 152 | 4.4 | ||||||||||||||||||||||||

| University System of Maryland | 4,699 | 0.8 | % | 146 | 5.9 | ||||||||||||||||||||||||

| Subtotal Top 20 Tenants | 433,116 | 73.3 | % | 14,982 | 5.9 | ||||||||||||||||||||||||

| All remaining tenants | 156,309 | 26.7 | % | 5,088 | 3.8 | ||||||||||||||||||||||||

| Total / Weighted Average | $ | 589,425 | 100.0 | % | 20,070 | 5.4 | |||||||||||||||||||||||

| Property Segment | Location | # of Properties | Operational Square Feet | Transaction Date | % Occupied on Transaction Date | Transaction Value (in millions) | ||||||||||||||||||||||||||||||||||||||

| 90% interest in MP 1 and 2 (1) | Data Center Shells | Northern Virginia | 2 | 432 | 6/2/21 | 100.0 | % | $ | 107 | |||||||||||||||||||||||||||||||||||

| Retired data center shell | Data Center Shells | Fort Meade/BW Corridor | N/A | N/A | 12/30/21 | N/A | 30 | |||||||||||||||||||||||||||||||||||||

| 2 | 432 | $ | 137 | |||||||||||||||||||||||||||||||||||||||||

| Total Rentable Square Feet | % Leased as of 12/31/21 | as of 12/31/21 (2) | Actual or Anticipated Shell Completion Date | Anticipated Operational Date (3) | |||||||||||||||||||||||||

| Anticipated Total Cost | Cost to Date | Cost to Date Placed in Service | |||||||||||||||||||||||||||

| Property and Segment | Location | ||||||||||||||||||||||||||||

| Fort Meade/BW Corridor: | |||||||||||||||||||||||||||||

| 560 National Business Parkway | Annapolis Junction, Maryland | 183 | 100% | $ | 66,325 | $ | 37,637 | $ | — | 2Q 22 | 4Q 22 | ||||||||||||||||||

| Navy Support: | |||||||||||||||||||||||||||||

| Expedition VII | St. Mary’s County, Maryland | 29 | 62% | 9,448 | 7,913 | — | 1Q 22 | 1Q 23 | |||||||||||||||||||||

| Redstone Arsenal: | |||||||||||||||||||||||||||||

| 8000 Rideout Road (4) | Huntsville, Alabama | 100 | 88% | 27,935 | 21,834 | 6,537 | 2Q 21 | 2Q 22 | |||||||||||||||||||||

| 8300 Rideout Road | Huntsville, Alabama | 131 | 100% | 51,100 | 18,786 | — | 4Q 22 | 4Q 22 | |||||||||||||||||||||

| 8200 Rideout Road | Huntsville, Alabama | 131 | 100% | 52,100 | 17,483 | — | 4Q 22 | 4Q 22 | |||||||||||||||||||||

| 6200 Redstone Gateway | Huntsville, Alabama | 172 | 91% | 54,827 | 16,121 | — | 1Q 23 | 1Q 23 | |||||||||||||||||||||

| 7000 Redstone Gateway | Huntsville, Alabama | 46 | 46% | 11,600 | 1,119 | — | 1Q 23 | 1Q 24 | |||||||||||||||||||||

| 300 Secured Gateway | Huntsville, Alabama | 205 | 100% | 59,700 | 3,128 | — | 1Q 24 | 1Q 24 | |||||||||||||||||||||

| Subtotal / Average | 785 | 93% | 257,262 | 78,471 | 6,537 | ||||||||||||||||||||||||

| Data Center Shells: | |||||||||||||||||||||||||||||

| Oak Grove C | Northern Virginia | 265 | 100% | 88,800 | 74,163 | — | 1Q 22 | 1Q 22 | |||||||||||||||||||||

| PS A | Northern Virginia | 227 | 100% | 65,600 | 6,279 | — | 2Q 23 | 2Q 23 | |||||||||||||||||||||

| PS B | Northern Virginia | 193 | 100% | 55,000 | 5,408 | — | 2Q 24 | 2Q 24 | |||||||||||||||||||||

| Subtotal / Average | 685 | 100% | 209,400 | 85,850 | — | ||||||||||||||||||||||||

| Total Under Development | 1,682 | 96% | $ | 542,435 | $ | 209,871 | $ | 6,537 | |||||||||||||||||||||

| Total Property | Square Feet Placed in Service | Total Space Placed in Service % Leased as of 12/31/21 | ||||||||||||||||||||||||||||||||||||

| Property Segment | % Leased as of 12/31/21 | Rentable Square Feet | Prior Year | 2021 | Total | |||||||||||||||||||||||||||||||||

| Property and Location | 1st Quarter | 2nd Quarter | 3rd Quarter | 4th Quarter | Total 2021 | |||||||||||||||||||||||||||||||||

7100 Redstone Gateway Huntsville, Alabama | Redstone Arsenal | 100% | 46 | — | 46 | — | — | — | 46 | 46 | 100% | |||||||||||||||||||||||||||

8000 Rideout Road Huntsville, Alabama | Redstone Arsenal | 88% | 100 | — | — | 9 | 11 | — | 20 | 20 | 100% | |||||||||||||||||||||||||||

2100 L Street Washington, D.C. | Regional Office | 59% | 188 | 107 | — | 81 | — | — | 81 | 188 | 59% | |||||||||||||||||||||||||||

Project EL San Antonio, Texas | Lackland Air Force Base | 100% | 107 | — | — | 107 | — | — | 107 | 107 | 100% | |||||||||||||||||||||||||||

610 Guardian Way Annapolis Junction, Maryland | Fort Meade/BW Corridor | 100% | 107 | — | — | — | 107 | — | 107 | 107 | 100% | |||||||||||||||||||||||||||

NoVA Office C Chantilly, Virginia | NoVA Defense/IT | 100% | 348 | — | — | — | 348 | — | 348 | 348 | 100% | |||||||||||||||||||||||||||

4600 River Road College Park, Maryland | Fort Meade/BW Corridor | 54% | 102 | 55 | — | — | — | 47 | 47 | 102 | 54% | |||||||||||||||||||||||||||

6000 Redstone Gateway Huntsville, Alabama | Redstone Arsenal | 100% | 42 | 32 | — | — | — | 10 | 10 | 42 | 100% | |||||||||||||||||||||||||||

| Total Development Placed in Service | 87% | 1,040 | 194 | 46 | 197 | 466 | 57 | 766 | 960 | 87% | ||||||||||||||||||||||||||||

% Leased as of 12/31/21 | 100% | 60% | 100% | 18% | 84% | |||||||||||||||||||||||||||||||||

| Location | Acres | Estimated Developable Square Feet | Carrying Amount | ||||||||||||||

| Land owned/controlled for future development | |||||||||||||||||

| Defense/IT Locations: | |||||||||||||||||

| Fort Meade/BW Corridor: | |||||||||||||||||

| National Business Park | 146 | 1,816 | |||||||||||||||

| Howard County | 19 | 290 | |||||||||||||||

| Other | 126 | 1,338 | |||||||||||||||

| Total Fort Meade/BW Corridor | 291 | 3,444 | |||||||||||||||

| NoVA Defense/IT | 29 | 1,133 | |||||||||||||||

| Navy Support | 38 | 64 | |||||||||||||||

| Redstone Arsenal (2) | 310 | 2,439 | |||||||||||||||

| Data Center Shells | 43 | 913 | |||||||||||||||

| Total Defense/IT Locations | 711 | 7,993 | |||||||||||||||

| Regional Office | 10 | 900 | |||||||||||||||

| Total land owned/controlled for future development | 721 | 8,893 | $ | 242,280 | |||||||||||||

| Other land owned/controlled | 43 | 638 | 3,453 | ||||||||||||||

| Land held, net | 764 | 9,531 | $ | 245,733 | |||||||||||||

| Wtd. Avg. Maturity (Years) (1) | Stated Rate | Effective Rate (2)(3) | Gross Debt Balance at 12/31/21 | |||||||||||||||||||||||

| Debt | ||||||||||||||||||||||||||

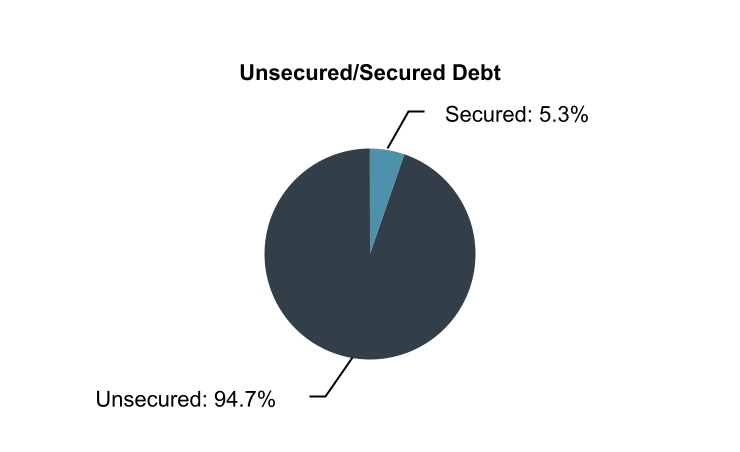

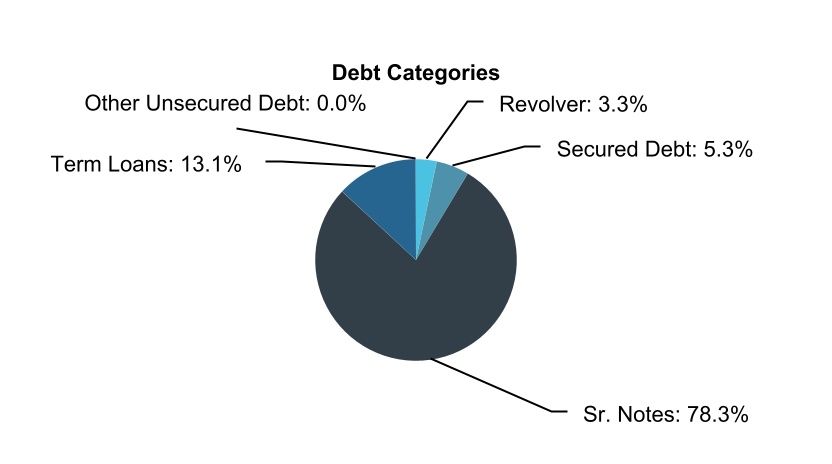

| Secured debt | 3.3 | 3.38 | % | 3.62 | % | $ | 121,425 | |||||||||||||||||||

| Unsecured debt | 7.0 | 2.27 | % | 2.64 | % | 2,176,861 | ||||||||||||||||||||

| Total Consolidated Debt | 6.8 | 2.32 | % | 2.69 | % | $ | 2,298,286 | |||||||||||||||||||

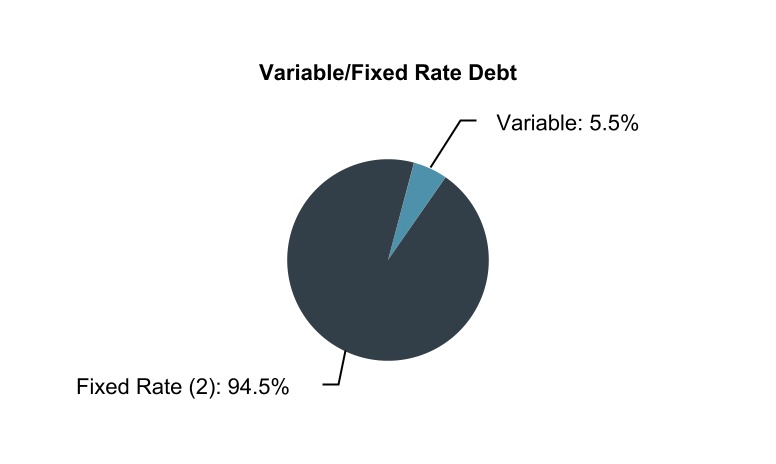

| Fixed rate debt (3) | 8.0 | 2.58 | % | 2.78 | % | $ | 2,172,286 | |||||||||||||||||||

| Variable rate debt | 1.4 | 1.16 | % | 1.16 | % | 126,000 | ||||||||||||||||||||